The NatGas Producer With The Best Chart Is Not Who You Think

![]()

The ESG trade of 2020-2022 made a lot of us a lot of money–it was one of the main memes of the Market, led by Tesla. But when meme soured, anything associated with ESG fell HARD–and RNG stocks were one of the worst sectors.

RNG is Renewable Natural Gas, which even today trades for 10x the price of Henry Hub ($35/mcf vs $3/mcf, roughly).

ANRG was $20+ back then! After nearly going bankrupt and being off the board for a time, it has re-listed and after a two week run lately where it is up 100%, now sports a near $500 M market cap, and is close to a 10-bagger since returning to the board.

It’s not the same company–a new strategic investor re-shifted the focus, and shareholders have done well by that. Here’s the full story:

QUICK FACTS

Trading Symbols: ANRG

Share Price Today: $2.87

Shares Outstanding: 170 million

Market Capitalization: $488 million

Cash: $43 million

Debt: $0 million

Enterprise Value: $445 million

A TURNAROUND IN THE MAKING

Anaergia (ANRG – TSX) is a throwback from BT – that’s Before Trump. A time when renewables were cool and their stocks were flying.

Anaergia is a renewable stock pure-play. They build waste-to-renewable natural gas (RNG) plants. They are very good at it.

But they’ve had a rough ride. This is a turnaround story. In 2021, the stock was $20+. Three years later it was a penny stock. Today it’s somewhere in between.

At its low, Anaergia came very close to bankruptcy. A year and a half ago Anaergia was out of cash. One of their key subsidiaries was actually in bankruptcy.

But Anergia found an investor to bail them out. Marny Investissment SA took an equity interest in the company in return for a $40.8M cash infusion.

It was enough to get the business back on its feet.

This year Anaergia has seen a string of big contract wins. The biggest came in early August when Anaergia was selected by a Spanish company in an engineering, procurement and construction (EPC) deal worth C$184M.

The stock has more than doubled since the beginning of this year.

Source: Stockwatch.com

The entire sector is seeing new life. Another biomethane stock, Greenlane Renewables (GRN – TSX), which we have owned and written about in the past, has also taken off. Greenlane went from 10c to 26c in just the last few weeks.

This post is mainly about Anaergia, but the questions I have could apply to either company: does today’s price ($2.55 a share for Anaergia, 26c for Greenlane) have more in it?

The answer is maybe. A lot will depend on whether these companies can secure even more work and begin to generate a profit. Because these companies are not the same as they were 5 years ago.

I’m going to take you through my reasoning below. But rather than just give you the dry details of what they do, I’m going to go by way of example.

We’re going to a dive into Anaergia by looking at what happened to their biggest failure – their large, flagship project, called Rialto. Doing so is going to educate on what they do, what they did wrong, and what is different today.

BUILD, OWN, OPERATE –

THE RIALTO RECIPE FOR DISASTER

Anaergia got in trouble by thinking big – and the Rialto Bioenergy Facility was the biggest.

Rialto is the largest project Anaergia has ever undertaken. It is the largest organic waste to fuel facility in North America.

Which is not necessarily a bad thing. But in their effort to think BIG, Anaergia relied on building facilities on their own dime.

They called the strategy Build-Own-Operate (BOO). This was really their go-to-public marketing schtick – We are going to build big bioenergy plants and become an industrial beheamoth.

In their Q2 2022 MD&A Anaergia described it as “Pursue Organic Growth and Shift Focus to Our BOO Segment”.

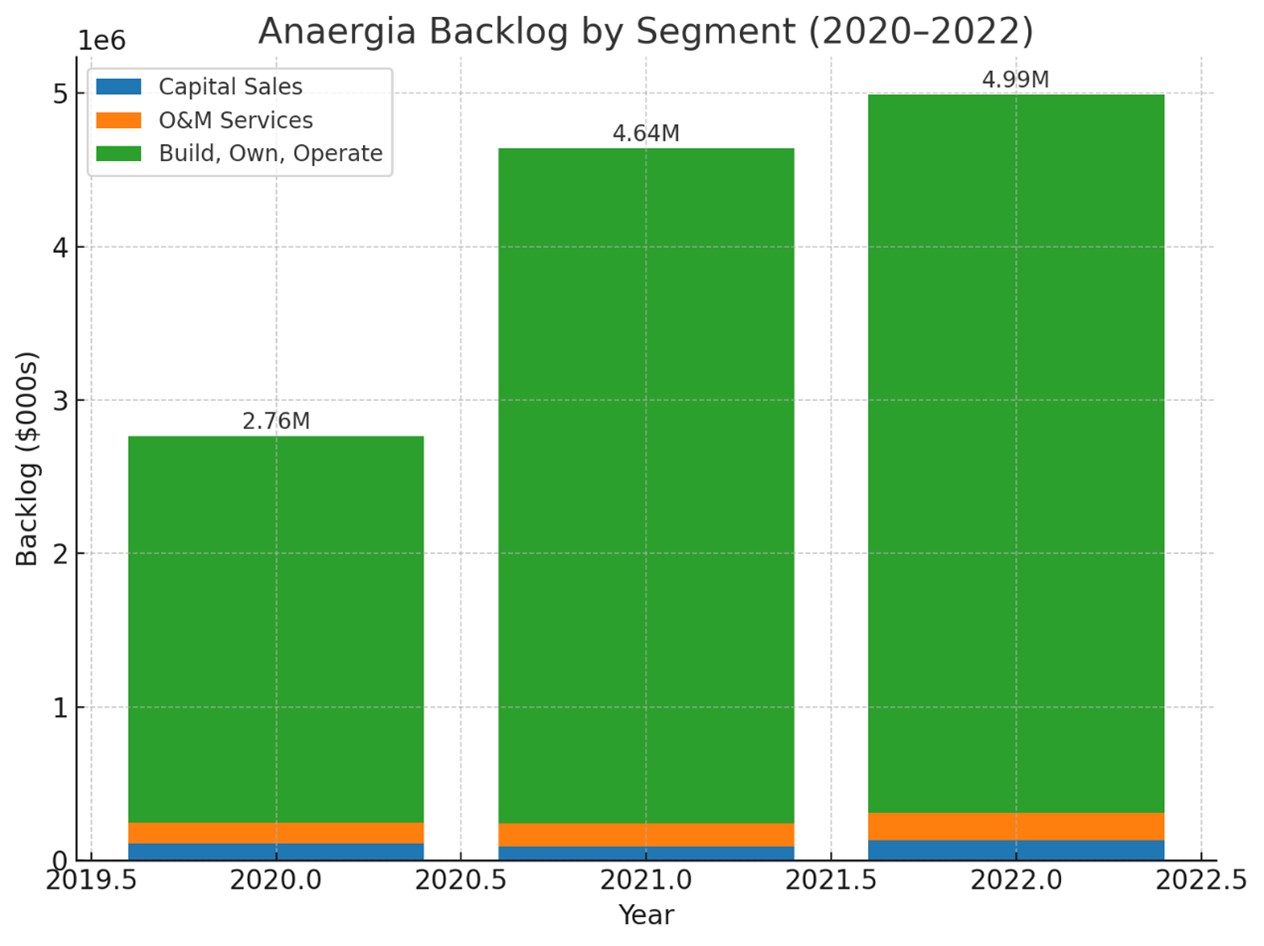

The BOO segment accounted for the vast, VAST majority of the backlog.

Source: Anaergia Financials

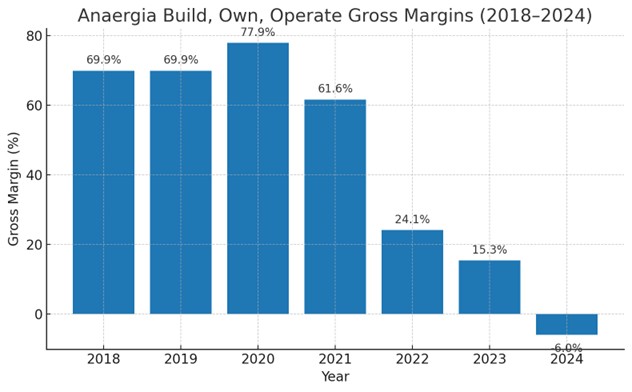

The focus was not without merit. Margins on BOO facilities were much, MUCH higher than their EPC business – 70%+ from 2018 to 2020.

But those margins unraveled when the business slumped.

Source: Anaergia Financials

The problem was that Anaergia was building BOO on their own dime, and taking on a lot of debt to do so. It left no room for error.

Which sent them reeling when Rialto began hemorrhage cash.

A BUSINESS THAT RELIES

ON GOVERNMENT LARGESSE

To best understand the Anaergia story, remember this key point – RNG plants get built because the government want them.

This isn’t meant to be a slight or a knock. It just is what it is. As an investor you need to understand the risk. RNG is built on subsidies and legislation (mostly climate related) that make this technology economic!

Rialto is a massive facility designed to stop methane emissions from landfills by diverting waste and converting it to renewable fuel.

Source: Anaergia.com

Rialto processes 1,000 tons per day (TPD) of municipal food waste, liquid waste, and biosolids. From that, they can produce over 1,000,000 MMBtu per year of carbon-negative RNG.

Let me stop here for a minute. That is the equivalent of about 2.7MMscfpd. That actually isn’t that much. The average output of a single natural gas well in the Montney is about 2-3MMscfpd. And that’s one well!

Consider that aerial photo. It is a MASSIVE plant–which produces the same amount of gas as a single gas well.

Say WHAT??? $160 Million capex vs $5 million capex. BUT…of course that well pays out twice—maybe—in its entire life. This gas plant goes on for decades. AND…RNG prices are 5-10x regular natgas—yes that’s right, 10x.

There are many companies willing to pay 5-10x for RNG vs regular hydrocarbons. In fact, this was big news back in 2020-2023.

But to get going–there is no way this facility is profitable without a whole lot of support.

It’s the Achilles heel of all these biomethane stories. They rely on government subsidies to get off the ground.

A recent IEA report put the price to produce for “90% of the potential [of RNG] at between USD 10 per gigajoule (GJ) and USD 30/GJ.” A GJ is roughly 1.05 MMBtu. That’s a natural gas price of $10-$30/MMBtu.

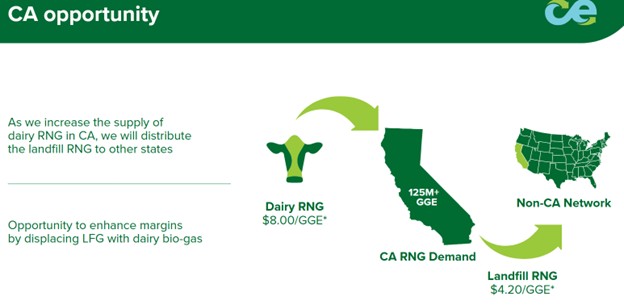

Which is why the Rialto facility was built in California. California offers big subsidies to producers of RNG.

The price of RNG from waste sources in California is about $4.20 per gas-gallon equivalent (this comes from Clean Energy Fuels (CLNE – NASDAQ).

Source: Clean Energy Fuels Investor Presentation

$4.20 per GGE is the equivalent of about $35 per MMBtu. Henry Hub prices are roughly US$3 now—so like I said, RNG is A LOT higher than the price of natural gas.

Nevertheless, it wasn’t the price of RNG that led to the downfall of Rialto. It was the feedstock, which came from Los Angelas waste, that did the facility in.

Here is where it is useful to get a bit of background on what exactly Anaergia does.

HOW TO PRODUCE GAS FROM WASTE

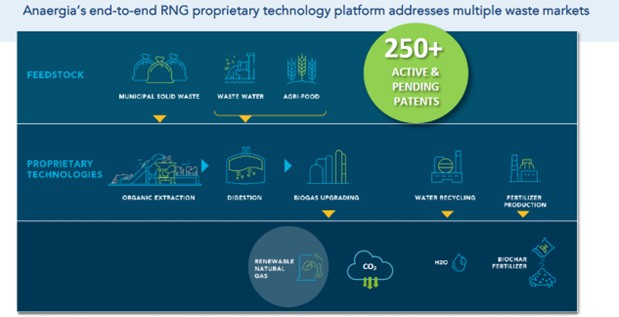

Let’s start at a high level: Anaergia converts municipal solid waste, wastewater treatment, agriculture and food processing waste into natural gas, fertilizer and water.

They take a waste stream, just about any waste stream, and subject it to anaerobic digestion.

Anaerobic digestion is what happens to waste in a landfill. Microbes break down the organic material, causing the complicated molecules in the waste (carbohydrates, fats, proteins) to turn into simple molecules, mostly methane and carbon dioxide.

The big difference is that in a landfill the process is “uncontrolled”. CO2 and CH4 go straight to the atmosphere. Anaergia instead captures the products and separates and purifies the natural gas stream into something that can be sold into a pipeline.

To go from what goes into our toilet to RNG takes some work. Extractors, digestors and upgraders are required to get to a final product that is 96-97% pure methane.

Source: Anergia Investor Presentation

Anaergia designs and manufactures a number of these.

Source: Anaergia Investor Presentation

All the parts are custom selected to work best with the waste being used, the location of the facility and other considerations. A lot of engineering goes into this. Anaergia is the EPC that can provide a full solution for a customer.

For those that remember Greenlane, they were a biogas upgrader. Greenlane focuses on a single step in the process, whereas Anaergia does the full waste to gas conversion.

Back to Rialto. Anaergia built Rialto in 2021. It took US$160M to build. To finance the project, Anaergia raised bonds (tax -exempt ones) through a California government supported financing, took out other loans (also guaranteed by the California Government) and contributed equity capital of their own for a 51% ownership.

The ownership structure kept Rialto separate from Anaergia in terms of a corporate entity, which turned out to be a very good thing, as Rialto filed for bankruptcy only a couple years later, in May 2023.

What killed the facility so quickly? The shit!

Rialto required food scrap and biosolid waste from the city of Los Angelas. There is a law in California, called SB 1383, that mandates organic waste diversion from landfill. It is an attempt to force cities to process their waste rather then just dump it.

I can only assume that while being environmentally better, it is a costly change for cities. Not surprisingly, Los Angelas delayed their enforcement.

This had a MAJOR impact on Rialto, which needed that feedstock to produce the RNG to sell to cover its debt.

From 2021 until 2023, Anaergia supported Rialto with debt and equity cash infusions. But something had to give. In mid-2023, Rialto was forced into bankruptcy.

The facility was eventually sold to Sevana Bioenergy for just $20M. Which could turn out to be a deal for Sevana. But that is of no help to Anaergia.

The bankruptcy of Rialto precipitated a wholesale change at Anaergia.

THE TURNAROUND –

FROM BUILD-TO-OWN TO EPC

In the summer of 2023 Anaergia initiated a strategic review. They sold other owned bioenergy facilities, mostly in Europe, to pay-off debt. The BOO backlog was eliminated.

In fact it was a 180 on BOO. Anaergia pivoted in favor of building projects for clients – a “Shift to Capital-Light Business Model”.

In their MD&A Anaergia now says they “plan to develop future projects with a financial partner who will fund all or the majority of the capital”.

Anaergia was also in need of cash. The Rialto debacle and other significant write-offs, not to mention a cash burn every quarter, left them scrambling for new investors.

Fortunately, they found one.

Last summer Marny Investissment SA made a $40.8M investment in the company and became the controlling shareholder with 60% ownership.

Marny installed what amounted to a brand-new team. Ohad Epschtein, a Managing Partner at Marny, because the Chairman of the Board. Assaf Onn was picked by Marny as the new CEO. And Gregory Wolf was picked as the new CFO.

THE BEST IN THE BIZ?

Why did Marney agree to invest in a struggling, unprofitable, low-margin, capital intensive project developer with a history of bankrupt projects?

Here’s the good news part of the story.

For all their struggles, Anaergia is very good at what they do. They push the envelope to develop new technologies and bring new plants into production.

These guys are simply the guys you call when you want to get a biomethane plant built. Best of breed.

They have deployed technology in over 230 resource recovery facilities in 17 countries since 2010. They have been involved with over 1,600 projects. They have built biomethane plants in Italy, Spain and California.

Here is a short list of highlights from their track-record:

• Rialto Bioenergy Facility – the largest organics-to-energy facility in North America.

• SoCal Biomethane Facility – Codigestion and biogas upgrading facility, also in California, won Global Water Award in 2023 for Wastewater Project of the Year.

• Agriferr Project – This was Europe’s first farm-to-BioLNG project, completed in 2022.

• Petawawa Project – Canadian showcase project that proved out retrofitting of existing wastewater digestion into net-zero carbon RNG production.

The bet here, both Marney and if you buy the stock, is simple: Anaergia made a misstep, they are course-correcting it, and they are good enough to turn it around.

Anaergia seems to have gotten back on its feet since moving in this direction. Nowhere is this more evident then in their backlog.

Anaergia had a backlog of $243.9M at the end of the second quarter. This is up from $103.1M at YE24.

Since the beginning of the year, they have won the following deals:

• A contract with Techbau to build 7 new Biomethane plants in Italy

• Letter of intent with JGC Holdings in Japan to supply technology and equipment

• Agreements with University of California to upgrade their Anaerobic Digestor

• A contract with City of Fermo in Italy to construct anaerobic digestion facility

• A contract with GWM S.a.r.l to provide two new biomethane plants in Italy

• A contract with Capwatt Biomethane Unipessoal, Lda to build a biomethane plant in Italy with a further 8 plants being contemplated

• A contract from New Jeju Bio Co. Ltd to design and build a biogas plant in South Korea

• An agreement with RDR S.p.A to supply capital equipment for Biomethane plant in Italy

And none of this includes their biggest deal – ever!

This particularly large project was signed mid-August. It is with a leading Spanish company that specializes in renewable natural gas projects where they have said publicly that they expect $184M of revenue.

The agreement covers building 15 new biomethane plants across Spain. This will include concrete tanks using the Triton digestor.

The Spain project is expected to be completed over the next 48 months.

CAPITAL LIGHT, MARGIN LIGHT

As I said before, the big change here is the focus on “capital light”.

What this means to the income statement is that Anaergia is a low-ish gross margin EPC business going forward.

For me that is the big takeaway. The difference between when I was looking at RNG stocks 4+ years ago and today is that these are now strictly EPC companies.

That means lower margin profile and lower profitability.

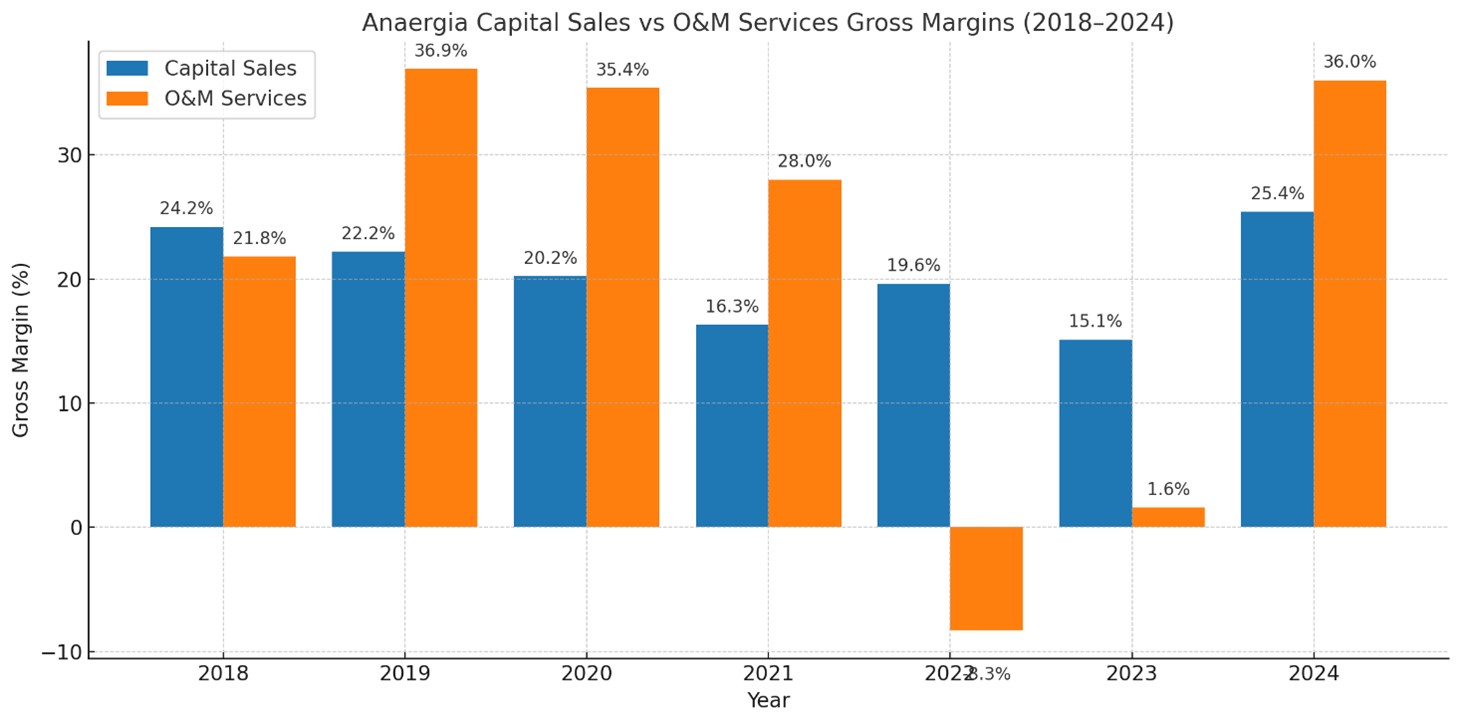

Apart from the two disaster years of 2022 and 2023 (when I assume margins were heavily impacted by write downs), Anaergia’s gross margins from their EPC segments (Capital Sales and O&M Services) have been relatively consistent.

Source: Anaergia Financials

Average gross margins in the Capital Sales segment have been 21.6% while O&M Services have been 31.6%.

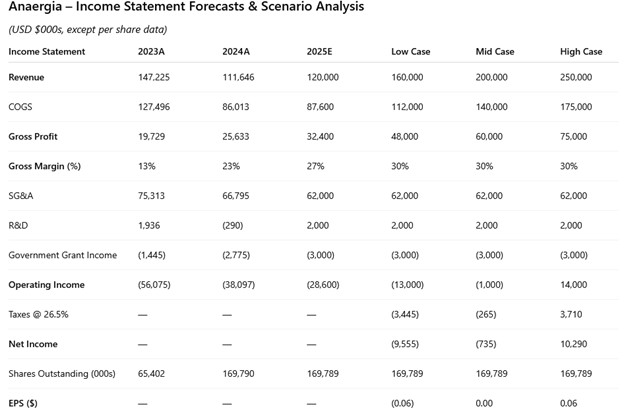

Plugging in these margins and existing operating expenses, you can get an idea of how much revenue Anaergia needs to generate to be profitable.

Source: Anaergia Financials, Our own Estimates

This is what makes me waffle. As the projections show, even at much higher revenue Anaergia is not super profitable.

Because of low gross margins and their ~$60M opex, Anaergia needs to generate a lot of revenue to overcomes that expense base.

Even at $250M of annual revenue, Anaergia will only generate 6c EPS (the current stock price would put them at 30x P/E based on 6c of earnings per share).

Of course, all this could change if Anaergia improves margins as they grow.

If I look over at Greenlane I see better margins and a much lower market capitalization.

Over the last 3Q’s, Greenlane has averaged 37% gross margins on their equipment sales and 50% on parts and services.

Greenlane’s trailing revenue is also a little over $40M, about 1/3 of Anaergia.

But Greenlane’s business is lumpy. Their quarterly revenue has been all over the map, with swings of +/-50% not uncommon.

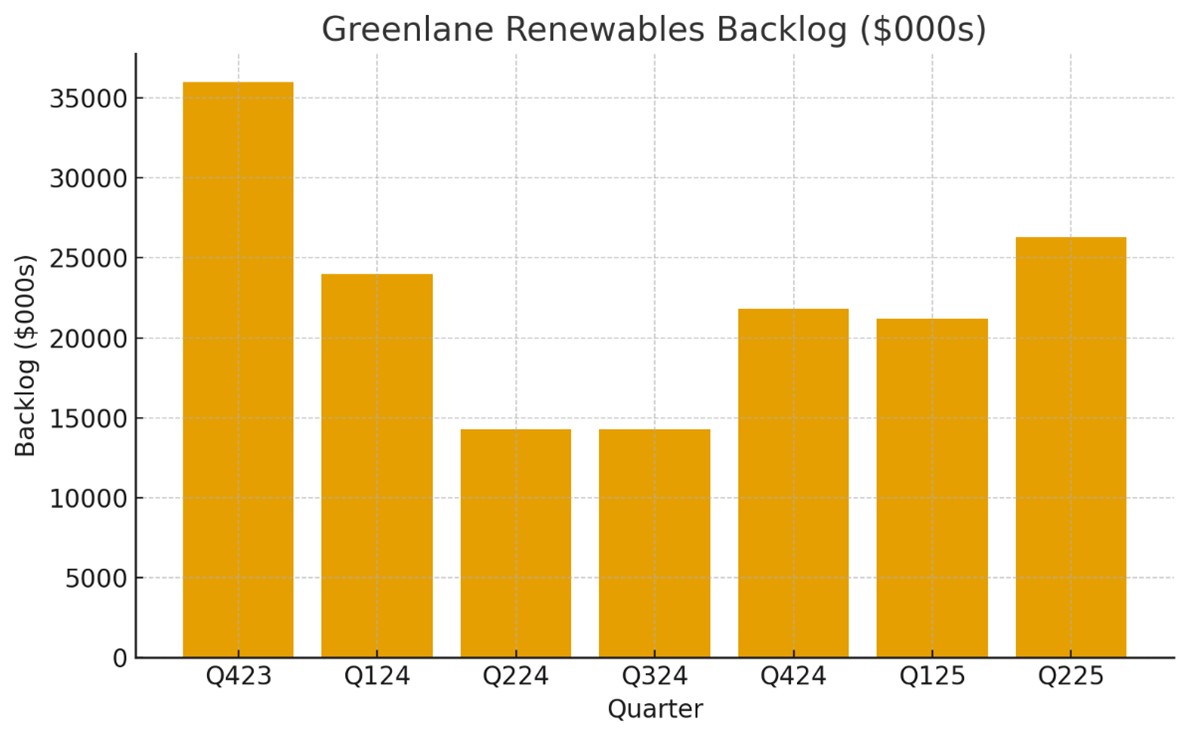

Much like Anaergia, Greenlane’s business has bottomed and is beginning to inflect.

Source: Greenlane Renewables Financials

For both these companies, more contract momentum and an increasing backlog is needed for the stocks to continue to work.

Which leaves me in limbo. While I am not going to argue whether the move in Anaergia has been justified, I will need to see more from the business to believe it can sustainably go higher.

Source: https://oilandgas-investments.com/2025/top-stories/the-natgas-producer-with-the-best-chart-is-not-who-you-think/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,745,414,074 |

| Stories: | 8,526,823 |

Whistler Blowers, Insiders