Is The Next Big Buyout in Canadian Resources COLONIAL COAL CAD – TSXv / CCARF-OTC

The writing is on the wall for Canadian listed Colonial Coal. On Nov 10 2025, CEO David Austen put out a press release saying talks had accelerated in his efforts to monetize shareholder value–which could come in the form of

- selling the company or

- selling just one of his two big assets

- partnering with a major or SEO–State Owned Enterprise

- or something completely different!

Austen sold Western Coal in the last decade for over CAD$3 billion. He’s a serious man and he has two seriously good and large coal assets in British Columbia. And rural Canada is desperate for employment.

The new federal Liberals under Prime Minister Mark Carney are clearly more business friendly than former PM Justin Trudeau (now known better for being Katy Perry’s boyfriend) so I see a clear path to a sale even if it’s to an Asian buyer. (Partha Sarathi Bhattacharyya, the former Chairman of Coal India, the world’s largest coal producer, sits on the board here.)

The stock just crested through $3 on Friday–more than double the $1.40 it was back on Nov 10. For disclosure, I jumped on this story for subscribers at $2.20 on Dec 22. I’m long 35,000 shares personally.

Now, in this world where large, high quality natural resources are being snapped up by governments in both East and West.

There is 695 million tonnes of METALLURGICAL coal (worth a lot more than thermal coal) here between Colonial’s two deposits in BC. If Austen gets $2 per tonne that equals roughly $8.75 cents per share. The Grassy Mountain metallurgical coal deposit in SW Alberta was sold in 2019 for over $3/tonne. That would be over $13 for Colonial Coal.

But this is not a slam dunk at all! Below you can read the full subscriber report from Dec 22 and understand why. But it’s a good speculation with one of the best management teams you could ask for.

QUICK FACTS

Trading Symbols: CAD-TSXV

Share Price Today: $2.20 (now $2.40!!!)

Shares Outstanding: 182 million

Market Capitalization: $391 million

Cash: $4 million

Debt: $0 million

Enterprise Value: $386 million

A MATERIAL CHANGE IN THE WORKS?

Colonial Coal (CAD – TSXv) has been in a holding pattern for years–but now the stock is running–faster than I can write a report! The stock is up almost 10% today but the takeout value here–which could be imminent if you read management’s last press release–still gives this stock a chance for a double to triple. (newsletter writer John Kaiser also wrote this stock up this weekend).

They have been sitting on two massive Tier-1 metallurgical coal assets in British Columbia. But the market couldn’t have cared less.

And why should it? Coal, especially coal in British Columbia, seemed like a non-starter.

Well, what can I say? – The times-they-are-changing!

With the new Federal government pitching big projects and with a renewed interest in coal (and a reduced interest in the climate), change could be afoot.

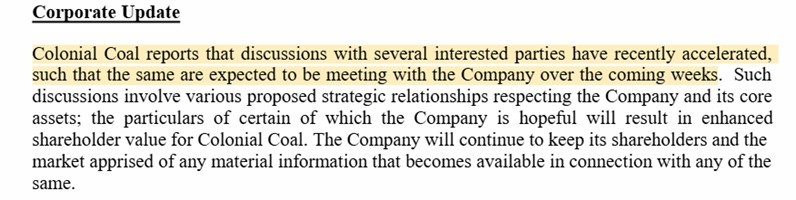

If I was just talking about another resource project that I hoped the government would fast track, this would be a wish and a prayer. But last week Colonial put out a press release with the following statement:

Source: Colonial Coal Press Release

Look, it is not unusual for a small company to put out this kind of press release, talking about early-stage discussions. But it is unusual for Colonial to put out a press release like this.

David Austin, CEO of Colonial, is a conservative guy. In fact, Austin has had run-ins with shareholders in the past about not disclosing enough. Austin has been accused of being too opaque, too slow, or too selective in what he discloses.

Colonial has not been promotional in the past. They have gone long stretches without saying anything at all. And now, here they are disclosing “several interested parties” and an acceleration of discussions.

Against that backdrop, this press release reads less like hype and more like intentional transparency.

On top of that, metallurgical coal prices are firm. Colonial noted that “current prices are in the range of US$200-230 per tonne”

Colonial stock has started to move but the company is still just trading at a fraction of its project NPV.

Source: Stockcharts.com

You add this all up and it becomes an interesting speculation. No guarantees, but one that could have a big pay off if it works.

COLONIAL COAL OWNS

A COUPLE OF POTENTIAL GEMS

Colonial coal owns two properties.

1. Huguenot

2. Flatbed (also called Gordon Creek)

Both of these properties host large reserves of metallurgical coal and could be extremely profitable – if they get built.

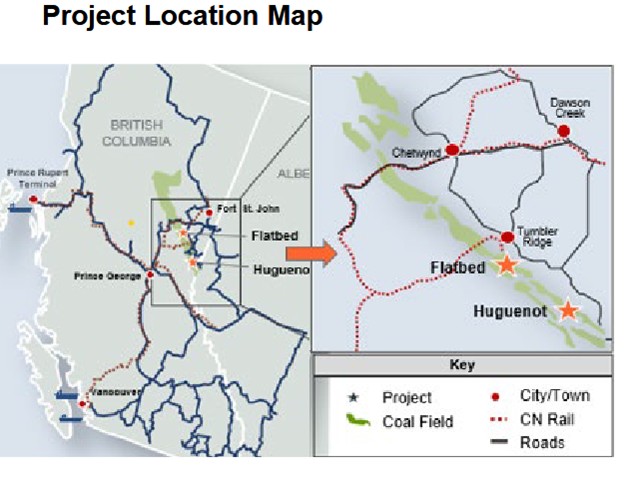

Both are located in NE British Columbia. Huguenot is 115 km SW of Grande Prairie, Flatbed is 131 km SW of Grande Prairie. There is access to rail, road and power, as well as being close to Tumbler Ridge, a coal town. Both projects are 100% owned by Colonial.

Source: Colonial Coal Investor Presentation

I’ll start with the basics on Huguenot, which is the flagship asset here.

HUGUENOT PROPERTY

Huguenot is materially larger (400 mt resource vs. 300 mt for Flatbed) and that resource has been drilled out to be largely measured and indicated whereas the Flatbed resource is inferred. The PEA of Huguenot estimates 89 Mt of coal produced over 31 years, whereas Flatbed is 57 Mt over 30 years.

Colonial had the PEA on Huguenot done by Stantec in 2018. This is an open-pit mine. There is an underground resource but that wasn’t used in the PEA.

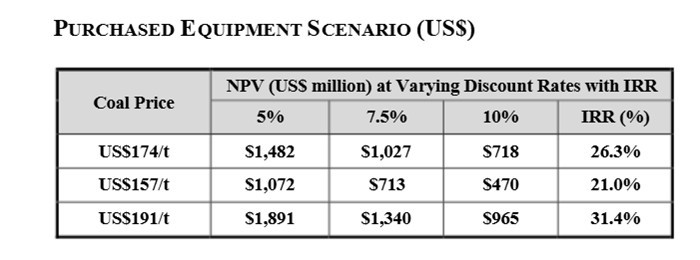

The NPV of Huguenot is BIG. Two scenarios were evaluated by Stantec, one that assumes Colonial purchases its equipment and another that assumes it leases its equipment.

Source: Colonial Coal 2018 Huguenot PEA

This is a high capital cost project. From the PEA:

Pre-production Capital Cost (purchased equipment): US$510M

Pre-production Capital Cost (leased equipment): US$303M

Huguenot capex is, at minimum, going to top C$400M, and it will be even higher if they decide to purchase equipment for the project. Also, these numbers from the PEA are 6+ years old, and inflation has certainly made them significantly higher now:

Mine cash costs are estimated at US$55 per tonne to US$ 61.50 per tonne, and full FOB port costs (basically including every cost until the ore is shipped) come in at US$91 per tonne.

These are decently low-cost numbers, so once that large capital amount is spent, the operating costs are going to make the mine solidly profitable.

Even at much lower met coal prices then we are seeing today, the mine is expected to generate significant cash. At a 10% NPV and using today’s prices, Huguenot should easily produce over US$1B of present value.

FLATBED PROPERTY

Flatbed is an underground deposit. It is not as far along as Huguenot, but it if Huguenot can get built, that alone would create a lot of value at Flatbed.

A PEA on Flatbed completed in 2019 estimated a US$446M NPV10 at US$160 met coal prices.

Source: Colonial Coal 2019 Flatbed PEA

The capex here is again significant. According to the PEA, Flatbed is going to require US$300M of upfront capex. Again this number is 5+ years old and is likely significantly higher today.

Flatbed should actually be a lower cost mine to operate than Huguenot. The PEA estimates all-in costs FOB port of US$81 per tonne.

BRINGING EVERYONE TO THE TABLE

The crux of the matter is this: these are profitable projects. The deposits would make a lot of money. The question has been the same one for the last decade: can these projects get built?

This is all about coal, the demand for it, the environmental impact, and getting approval from all parties involved.

Let’s start with where they are located. Both properties are on Treaty 8 territories and in British Columbia. Neither is permitted as of today, and neither has an impact benefit agreement (IBA) signed, which you need to move forward with the First Nations whose traditional territory may be affected.

Being on treaty land means that provincial and First Nations consultation is a requirement. Being in British Columbia means that the government must approve.

If Colonial makes steps to get these projects shovel ready, it is going to mean going through the B.C Environmental Assessment office (EAO), engaging and getting Treaty 8 nations onboard – in other words, its going to be a process.

That doesn’t mean it is impossible. The Murray River coal project was approved nearby in 2018. Murray River is an underground met coal mine owned by the private company HD Mining International.

The tribes involved seem to be engaged in resource development. I see opinions on both sides, but it doesn’t seem like getting an IBA signed is insurmountable.

With that in mind though, Murray River is also a bit of a cautionary tale. Even though approved, the project began construction but was put on care and maintenance earlier this year.

HD Mining blamed tariffs and the price of coal.

Unfortunately, because HD Mining is privately owned, there isn’t an available PEA to compare to Colonial’s projects. We do know from news reports that the upfront capex was expected to be around C$700 million, which is in the same range as both Colonial mines.

The risks here are more than just getting all parties onboard.

THIS IS AN ALLSTART TEAM UP TO THE FIGHT

What Colonial has on its side is a team that knows met coal.

That starts with David Austin. Austin is a long-time expert in the coal business. He co-founded Western Coal Corp., a major metallurgical coal developer that sold to Walter Energy in 2010 for approximately C$3.3 billion.

On the board is Greg Waller, a long time Teck VP that retired after 33 years. Next is Partha Sarathi Bhattacharyya, the former Chairman of Coal India, the world’s largest coal producer. COO John Perry has a long history of coal exploration.

It’s a team of heavy hitters with lots of coal experience.

COULD IT BE A GO?

I’m not going to sugar coat it. Colonial Coal is no sure bet. But if there is something to these rumors that the project is getting off the ground, the valuation could go higher.

With 182M shares outstanding the stock is trading at a market capitalization of C$360M. The NPV of these projects are more than triple that amount.

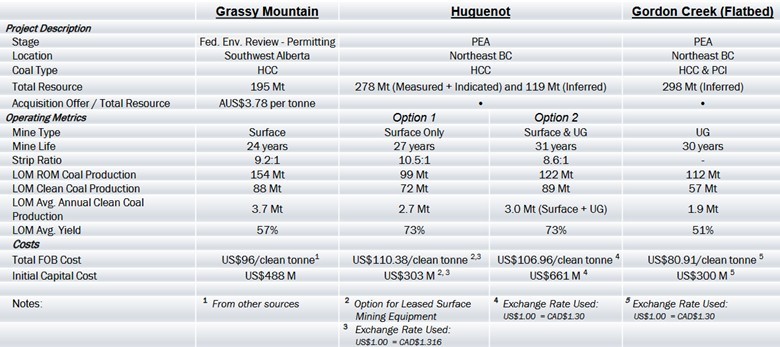

Colonial provides an interesting table in their investor presentation that compares their two projects to the Grassy Mountain project in the Crowsnest Pass.

Source: Colonial Coal Investor Presentation

If you take the Grassy Mountain acquisition price of AUS$3.78 per tonne of resource and apply that Huguenot, you are looking at well over C$1B. Flatbed adds almost another C$1B.

But Grassy Mountain is also its own cautionary tale. The opposition to this coal mine in Alberta has been fierce. There has been a grassroots campaign, environmentalists involved, and musician Corb Lund leading the charge (he’s in the process of getting a petition submitted to reject the project). While the Alberta Government wants this mine built, there still is no guarantee it gets done.

Colonial faces a somewhat bigger battle. The BC government in power today is not going to be as friendly to coal.

Nevertheless, my gamble here is that Austin wouldn’t be putting out this kind of press release if there wasn’t a reason to. And if that’s the case, then I expect these early negotiations materialize into something meaningful.

You follow that up and the stock should continue to rise as it becomes more likely that at least one of these projects (likely Huguenot) is going to get built.

It is a gamble, for sure. But one I am willing to take.

Source: https://oilandgas-investments.com/2026/latest-reports/is-the-next-big-buyout-in-canadian-resources-colonial-coal-cad-tsxv-ccarf-otc/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,825,636,537 |

| Stories: | 8,677,206 |

Whistler Blowers, Insiders