The Cheap, Very Odd Bank That’s Run By The Tim Hortons Founding Family

QUICK FACTS

Trading Symbols: RFA-TSX

Share Price Today: $24

Shares Outstanding: 46.6 million

Market Capitalization: $1.1 Billion

Tangible Book Value: $1.497 Billion

FINDING THE CHEAT CODE FOR BANK GROWTH

RFA Financial (RFA – TSX) is one of those stories that gets more interesting the longer you look at it. Yesterday, they just reported their first ever quarterly as a combined bank/REIT–odd combination yes?–and while the numbers (and the transparency) were not great, this is a bank stock that is really cheap and has some very entrepreneurial backing.

It came to my attention as the Joyce family, who turned Tim Horton’s into a Canadian icon brand, are the major shareholders. Oh, and they bought a REIT….????

At first glance, it looked like a pass. It’s a Canadian bank. No branches. Depends entirely on GICs for deposits. Lends almost entirely into residential mortgages. And the loans it makes are further down the ladder than the Big 6 banks. RFA specializes in alternative lending to borrowers who wouldn’t qualify for a loan from the bank. Which means risk.

You add all that up and you sort of go – eh… But you can’t just stop there.

Because here’s the twist. RFA just completed the acquisition of Artis Real Estate Investment Trust. This was a reverse take-over, with RFA taking over the combined businesses.

Once you understand why they did it, the story changes completely.

Combining a bank and a REIT seems a little odd. It is odd! Banks are usually trying to get rid of the real estate, which they get from loans that go bad. Regulators actually forbid banks from owning too much real estate. RFA had to ring fence the Artis assets to make the acquisition work.

So a bank deliberately going out and acquiring a REIT? It’s simply not done!

But there is method to the madness.

On the surface, this looks like RFA acquiring a bunch of real estate. But what is really going on here is far more interesting – RFA is acquiring capital at a discount.

That changes the story entirely. It makes the upside of RFA Financial more compelling. And it may make the stock itself a buy.

HOW DO YOU GROW YOUR BANK FAST?

The fundamental constraint of any small bank is capital. To make more loans, you need more equity on your balance sheet. If you don’t have the equity, OFSI (the Office of the Superintendent of Financial Institutions, which is the independent regulator of banks in Canada) is going to rein you in.

getting capital isn’t easy. You need a willing buyer of your equity, and unless you are willing to throw your existing shareholders under the bus, they need to give you that equity without asking for a big discount.

Otherwise you grow within your means. Which is what most banks do – use their own earnings to grow the business. That’s why banking is generally a boring business to invest in – it is a multi-year process of compounding capital at modest rates.

With the acquisition of Artis, RFA has found itself a cheat code to this slow, growth-within-your-means, problem.

THERE’S LEVERAGE, AND THEN

THERE’S BANK LEVERAGE

Here’s how RFA explained it on the day of the deal: they plan to unlock value within the real estate portfolio and recycle that capital into higher-return financial services investments.

Bank-speak right? But parse it out and you have a genuinely elegant growth strategy.

Artis owns a lot of real estate, which RFA just purchased at a discount to book. RFA plans to sell that real estate down over time. They believe that they can sell that real estate at or above book value.

If they can, the math maths.

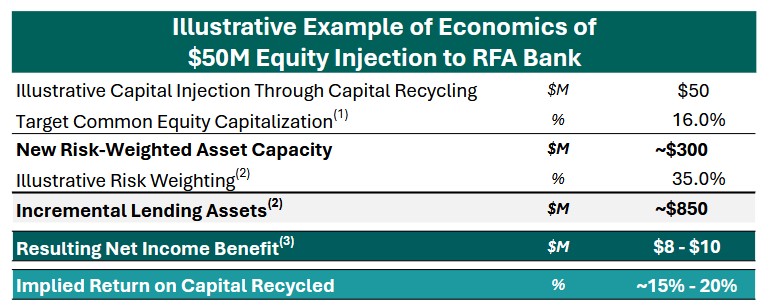

The real estate that Artis owns comes with its own mortgages. When RFA sells a parcel of real estate, they pay off the mortgage. The rest – the equity – becomes fresh capital for RFA Bank.

As of Q3 2025, Artis maintained a debt to book value ratio of 42%. That means for every $1 of property value, there is 42 cents of debt. The other 58 cents is equity. Sell a building at book and RFA gets 58 cents of every dollar on their balance sheet.

The magic is what happens next. The new equity can be levered because RFA is a bank.

Before the acquisition RFA had $2.7 billion of total assets. They had $308 million of equity. They were levered at about 9:1.

Artis had real estate that was levered at >2:1 (remember there was about 58c of equity for every $1 of property value). That $1 of real estate equity, once recycled into the bank, can support roughly 4x as many new loans.

RFA believes they can achieve a return of 15%-20% on the new equity.

Source: RFA Business Combination Presentation

Of course, to pull this off, RFA needs to have its entire business ramping. Beginning with their deposit base.

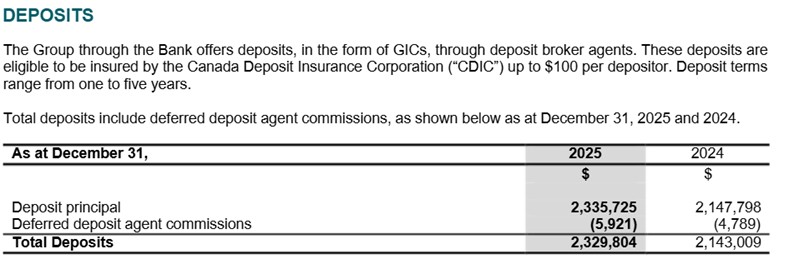

THE DEPOSIT SIDE: BROKERED GICS

To fund that new lending, RFA needs to grow deposits.

RFA has no branches. No retail banking customers. Instead, they raise money by selling GICs — Guaranteed Investment Certificates — through a network of independent investment dealers. These are called “brokered deposits,” and they are, frankly, the most efficient deposit model in banking.

No branches mean no branch overhead. No retail customers mean no customer service army. You’re essentially a wholesale funding operation that happens to be a bank.

RFA’s entire deposit base of GICs was $2.3 billion at year-end 2025.

Source: RFA Annual Report Statement

Those GICs most often carry a 1–3-year duration. As the Bank of Canada has cut rates, RFA’s average GIC cost has fallen from 4.5% to around 3.7% over the past year.

Source: RFA Annual Report Statement

To grow, RFA will need to pay up for deposits. And they will. If you scan GIC rates online right now, you’ll notice two buckets: the well-known banks offering around 2.5%, and a second group — Home Trust, Fairstone, Versabank, RFA Bank — offering something closer to 3.3% for a one-year term. These are the lenders willing to pay for deposits because they need them to grow. RFA is squarely in that camp.

THE LOAN BOOK – SIMPLE, BUT NOT WITHOUT RISK

The second, and rather obvious thing that RFA needs to do to take advantage of this newfound capital is to make more loans.

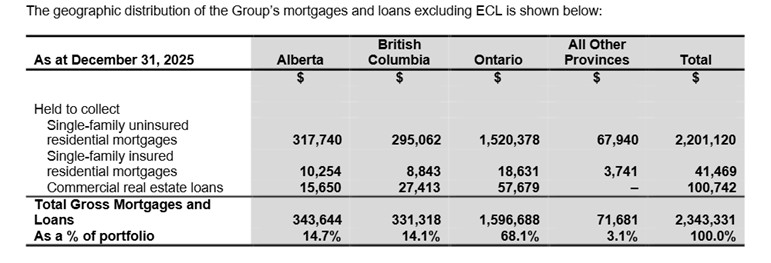

Just as RFA’s deposit bank is simple, so is their loan book. Over 90% of their loans are single-family uninsured mortgage loans.

Source: RFA Annual Report Statement

Of that, about 70% of the loans are in Ontario. The rest is almost evenly split between Alberta and British Columbia.

These are Alt-A and B mortgages – loans for borrowers who don’t qualify for insured or prime lending. Because they’re uninsured, they can’t be packaged through NHA MBS/CMB. They have to be funded with deposits and held on the bank’s balance sheet.

What kind of borrowers are these? Self-employed, bruised credit, new to Canada, non-standard income. These are higher-risk loans. But RFA gets paid more to carry them.

In 2025 RFA earned $158.7 million of interest income on assets that averaged around $2.7 billion over. That’s a yield of 5.9%. Their residential real estate loans average a shade over 6%. Even with higher deposit costs, which are over 3%, RFA generates a decent interest spread with these loans.

To generate more loans, RFA will rely on their mortgage broker network.

These mortgage brokers don’t work for RFA. They are simply looking for the best mortgage deal for their clients. RFA compensates them for delivering oans.

Their reliance on 3rd party brokers could be a governor on growth and RFA knows that. On the call where they discussed the acquisition, RFA management said that to accelerate the growth, the would look at buying up loan portfolios in addition to expanding organically.

THEY’ll HAVE TO MAKE SOME DEALS

The third and final, piece of the puzzle is the capital. The capital only materializes if RFA can sell the real estate at an attractive price.

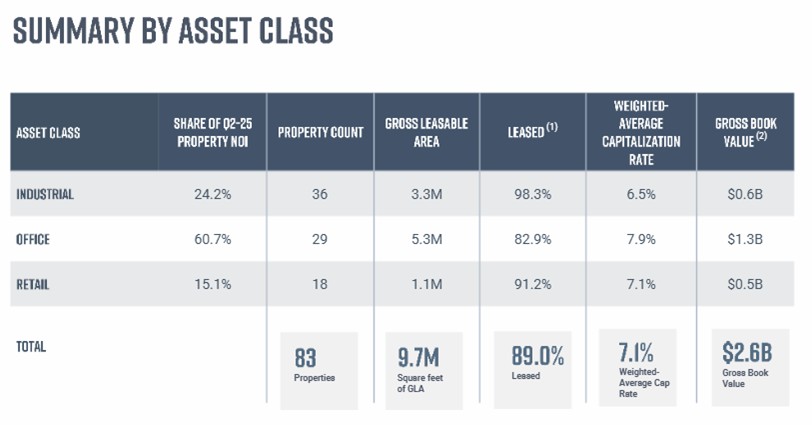

The portfolio they are working through is substantial: 10 million square feet across 92 properties in Canada and the United States. There is industrial, retail, multi-family and office properties in the mix.

The biggest reason that Artis was trading at such a discount to book were its office properties.

That last one is critical. Office.

Artis, now RFA, owns 29 office properties. Of that, about 55% of their leasable area, and 61% if their operating income came from office properties.

Source: Artis REIT September Investor Presentation

Office is about half of the book value. It’s got to be the biggest question going forward – can RFA sell these office buildings at or near that book value?

Artis has demonstrated that they can sell assets – they have sold approximately $1.5 billion at near book value over the past 2 years.

But honestly, that doesn’t really tell us much about what is left. Each property is sold on its own merits.

For example, we won’t know what the Artis office buildings in Winnipeg, where they own 8, or the 15 buildings they own in Madison Wisconsin, can be sold for until they are sold.

Winnipeg’s office market is functional but not healthy — vacancy is elevated and net effective rents on new leases have been weak.

Source: Colliers Winnipeg Q126 Report

Madison looks better: vacancies in the single digits, rents nudging up.

Source: Cushman and Wakefield Madison Q126 Update

Artis has been disposing of office properties. They sold one in 2025:

Source: Artis REIT MD&A

They sold 8 in 2024.

Source: Artis REIT MD&A

Unfortunately finding out how much each of those sales went for, specifically how each of the individual sale compared to book value, is not possible because that information isn’t the sort of thing that is published.

THE OTHER REAL ESTATE RISK

The other uncertainty here are the residential loan book and making even more of them in the current environment.

Canadian real estate has cooled meaningfully from its 2021-22 peaks. Delinquencies are rising across the board, and alt lenders tend to see that stress first because their borrowers have less financial cushion.

RFA’s borrowers — the self-employed, the new arrivals, the ones with lumpy income — aren’t bad credit risks by definition. Many of them just don’t fit the rigid underwriting box that the big banks use. But statistically, they are more vulnerable to income disruption than a salaried employee with a T4.

The LTV structure is the safety valve of alternative borrowing. An alt borrower who put 25% down has to see property values fall 25% before the bank faces any principal loss.

Unfortunately, we don’t have that information yet. This is an RTO and all we get is an investor presentation and the financials.

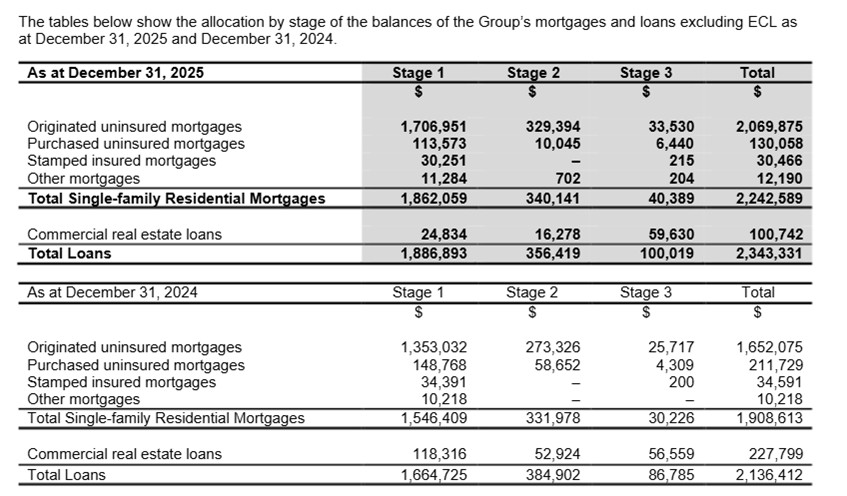

What we do know is that their loan book is largely current, and that defaults don’t seem to have risen materially year-over-year.

Source: RFA Annual Report Statement

Loans in Stage 3 are in default. Loans in Stage 2 have had some sort of trouble, they call it an increase in credit risk. Stage 1 loans are fine. There isn’t really a notable change in the Stage 2 and Stage 3 loans here after accounting for the fact that the entire loan book has grown almost 15% year-over-year.

IT’S ALL PART OF THE PLAN

What I’m outlining above is a bank that has some heavy lifting ahead of it.

Which is why it is important to realize that RFA is not just some random upstart bank hoping to hit it big.

RFA is 23% owned by Steven Joyce and his company Halycon.

Joyce’s name may sound familiar. He is the son of Tim Horton’s Founder Ron Joyce.

Halycon is a private investment company that has been largely funded from the Tim Horton’s windfall.

Joyce and Halcyon weren’t just passive participants in the merger. In fact, Joyce had stakes in both RFA and Artis prior to the merger.

The same can be said for the CEO of RFA, Ben Rodney. Rodney was CEO of RFA and he was the Chairman of the Board of Artis.

Clearly the big players involved here know what they are combining and they have a plan of how they want this to go down.

WHERE DOES THIS ALL LEAVE US?

When the merger closed RTA consolidated shares on a 3:1 basis. Artis shareholders received 31.7 million shares, RFA holders got 14.9 million.

RFA’s own book value was $270 million pre-acquisition. So on a per share basis, it was about $18 on a post-consolidation basis. The stock trades at $24 today, so a premium to book.

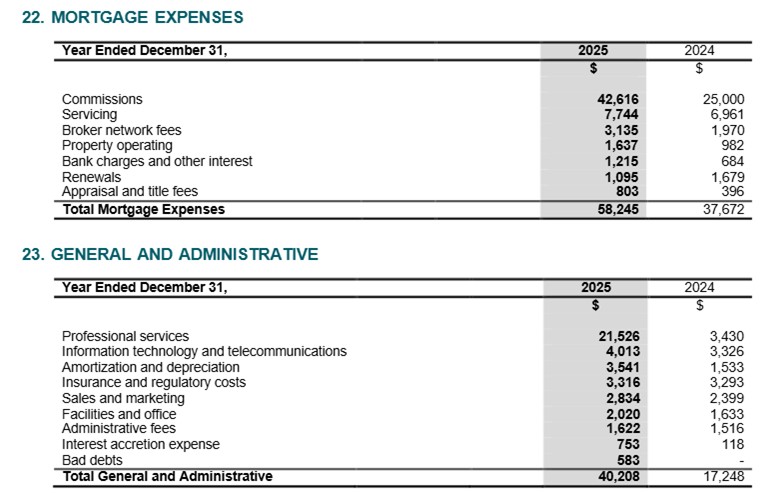

The operating performance before the merger is harder to read. RFA lost $29 million in 2025 after making $17 million the previous year. They saw much higher operating expenses year-over-year even on essentially flat net revenue.

Drilling down on those expenses, the two big increases came from commissions and professional services.

Source: RFA Annual Report Statement

I don’t know why commissions were so much higher in 2025 when RFA’s loan originations were just up a bit from 2024. I also don’t know if the big increase in professional services were because of the Artis merger, or something else?

Again, because this is a newly public company via RTO, there isn’t a deep well of public disclosure to explain the swing.

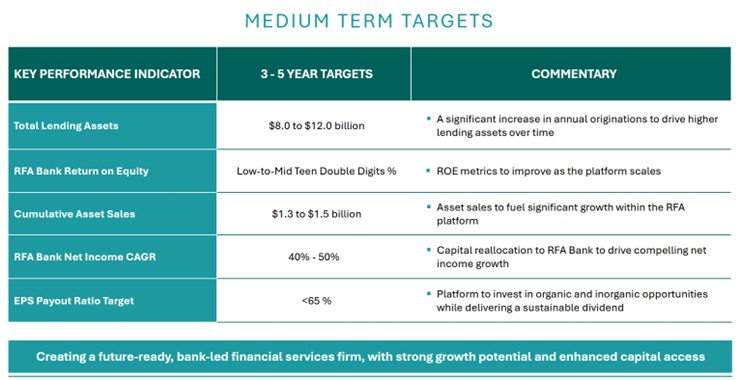

What RFA has laid out is a plan for growth.

Source: RFA Business Combination Presentation

Their 3–5-year target of $8-$12 billion of lending assets is 3-5x more than today. Their goal of 40%-50% net income CAGR would exceed even the most aggressive banks out there.

Run the math on that ROE target. Combined equity of roughly $1.5 billion. A 13% ROE gets you to about $200 million of net income — or $4.30 per share. Against a stock price of just over $24, that’s a price-to-earnings multiple of less than 6x. On target numbers.

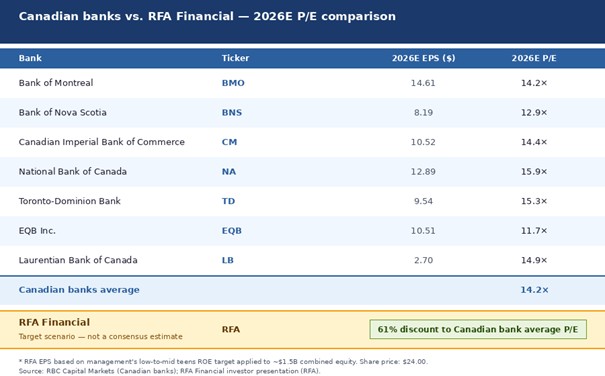

Below is a comparison of these pro-forma RFA numbers versus 2026 estimates from RBC of other Canadian banks.

Source: RBC Capital Markets

The comparison makes RFA look pretty darn cheap. The reason for the discount is simple. RFA has to realize the asset sales, raise enough deposits to finance them and make the loans before they can realize that ROE.

Each of those pieces is achievable. None of them is guaranteed. But if you believe management can execute — and the early evidence is encouraging — the stock at $24 is pricing in a lot of skepticism that may not be warranted.

Which could be a very good reason to own it here.

EDITORS NOTE—My latest subscriber pick is a small cap turnaround with a unique business model–revenues are increasing, and it generated positive EBITDA last two quarters. A new CEO with skin in the game is getting the business and the stock moving. Get my full report–SUBSCRIBE HERE

Source: https://oilandgas-investments.com/2026/latest-reports/the-cheap-very-odd-bank-thats-run-by-the-tim-hortons-founding-family/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,825,428,469 |

| Stories: | 8,676,659 |

Whistler Blowers, Insiders