Are Investors Returning to Gold Stocks?

Source: Adrian Day 09/08/2025

Global Analyst Adrian Day looks at a possible change in the gold market, as well as reviews the last quarters earnings reports for clues as to the next quarters winners.

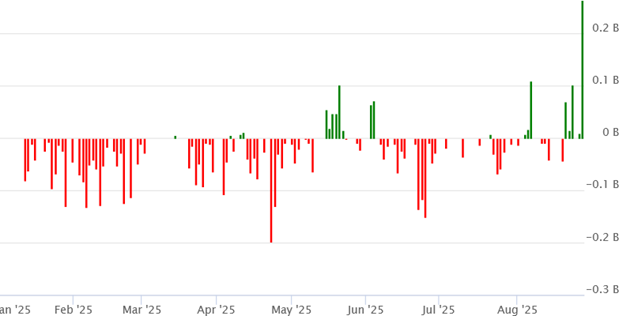

Finally! Over the past week, there have been flows into gold funds, and in scale, after long periods of outflows. The stocks responded, up over 8% on the week. Is this the beginning of the next phase in the gold bull market? We have long discussed how North American investors have largely been absent from this bull market.

Massive gold buying has come from central banks, from Chinese investors, and from wealthy Middle Eastern and Asian families, all for their own reasons. The traditional economic factors that have drive North American investors — a weakening economy, low and declining interest rates, high and rising inflation, and a weakening dollar — have mostly been absent over the past three years as the gold price has appreciated by over 110%. The dollar fell sharply in the first half, but the economic narrative, until recently, was still positive.

US Gold Investors Have Been Absent

But because different groups of global investors were buying gold for their own non-economic reasons, they were buying the physical metal and not North American gold stocks. North American investors who are the main buyers of North American gold stocks were largely absent from the market, as I have discussed here (see inter alia, Bulletin #964), and on many recent interviews (here); it was even the topic of my talk at Rick Rule’s Boca Symposium in July (“Sherlock Holmes and the Case of the Missing Gold Investors”).

Until last week, the GDX fund of major gold miners (and royalty companies) saw $3.5 billion of outflows, while the GDXJ of supposed “juniors” (more like intermediates) had $1.2 billion flow out. For funds with total assets of $19 billion and $6.6 billion respectively — after the strong rallies — these flows out are not insignificant.

North American investors were not interested, even in physical gold. After the bottom in October 2022, until this year, the major gold bullion fund, GLD, saw over $5 billion in outflows. There has been some interest this year, but hardly a gush, and in fact interest has waned as the year rolled on. In the first four months of this year, there was almost $7 billion of inflows, but in the last four months, only $2.85 billion.

Finally, Inflows into the GDX

But last week this changed. Daily inflows into both funds, nearly half a billion for the GDX, are hopeful signs of a shift. One swallow does not make a summer, and one week does not dictate a change in trend, but the shift has come for fundamental reasons, not just random factors. That the economy is slowing is becoming more apparent; the weakness in the labor market is difficult to ignore.

FedHead Jerome Powell talked a week ago about “adjusting our policy stance” with markets (per Fed Funds Futures) over 90% betting on a cut at the Fed’s September meeting. And this, even while consumer and producer prices have been moving up. The economy is clearly turning towards an environment that is conducive to gold. Perhaps too the S&P will weaken; Nvidia Corp.’s (NVDA:NASDAQ) fell Friday, wiping out a month’s gains as it failed to exceed impossible-to-meet expectations for the stock. Investors are finally paying attention.

Gold Stocks Still Have Leverage Over Bullion

The moves last week clearly show us what might happen to the gold stocks if investors turn back to the sector. Although the stocks have clearly performed well this year — blithely and stealthily outperforming the S&P ninefold — they still have not exhibited their traditional leverage to bullion, lower than two-to-one over the past year, compared with, for example, 3.4 x the last time gold moved up 40%. We have a lot further to go; the XAU is still below its 2011 peak, while some individual names are well below; Newmont Corp. (NEM:NYSE; NGT:TSX; NEM:ASX) would have to move more than 30% just to reach its end-2022 high, while Barrick Mining Corp. (ABX:TSX; B:NYSE) would have to double to reach its 2011 high.

And more importantly than the price, the value remains good, by many metrics well below long-term average valuations. As the gold price has moved up, so has the value of gold reserves, so too have the margins expanded and the cash flows increased, often at a greater pace than the gold price itself has appreciated. Thus, the stock valuations have remained low.

But with stocks up an astonishing 86% so far this year, one needs to be a little more discriminating as one invests in the sector going forward.

The Lessons To Draw From Recent Financial Results

With second-quarter earnings for the gold companies now finally behind us, we can draw some lessons as we look ahead. We can look at how stocks reacted to earnings results and why, and see what we learned in Q2 portends for Q3. What was the market expecting and what did it get? What concerns did the market have and how were they addressed?

First, let’s review briefly results for the group. We saw record revenue and free cash flow across the board, with companies strengthening balance sheets — most now being net-cash positive — and some

buying back shares and increasing dividend payouts. Costs were mainly under control, though there were unexpected increases at some. Despite one or two individual problems, and a couple of misses on guidance, all companies reiterated full-year guidance, with many being second-half weighted. The royalty companies in particular generated massive cash flows allowing them to make new deals while adding to cash piles.

Most Companies Beat Expectations on Higher Gold Prices

It was a strong quarter, with 26 of top 34 companies beating consensus earnings estimates, but even those that did not beat for the most part still had solid quarters. Higher gold price were largely responsible: the average gold price in the second quarter was $3,286, up 15% on the first quarter ($2,862). If a company’s results were due solely to higher gold price, then clearly a look at how gold is doing becomes critical. This quarter, the gold price is averaging just over $3,350, a few percentage over Q2. The price has been range-bound since mid April. But let’s remember that the second quarter includes early April when the gold price was as low as under $3,000. So even if the gold price remains flat for the rest of this quarter, the average price will be appreciably higher.

Production and costs were largely as expected. Overall, production was up very marginally for the large miners, while the largest actually reported declining gold production last quarter, notably Newmont and Barrick, down 8% and 16%, a continuation of long-term trends for both, hence Newmont’s acquisition of Newcrest and Barrick’s pivot to copper.

Why? Large mines are depleting assets. In addition, Barrick lost its Mali contribution while Newmont lost ounces from the mines it sold. Most of the growth came in the smaller mid-tier gold miners in the bottom half.

Costs Under Control

Another important factor for companies with meaningful non-gold production. If they report Gold-Equivalent Ounces (“GEOs”) then production can show a decline as copper, oil, and so on are converted into a much-higher gold price. This is significant for Franco-Nevada Corp. (FNV:TSX; FNV:NYSE), for example, as its Q2 GEOs for its large oil and iron ore investments fell, leading to an overall company drop in its headline GEO production.

Cash costs, at $1,186, were up15% year-on-year while AISC fell 10% to $1,424. These are still good numbers, but remember the averages include the royalty companies which distorts the cost picture. In addition, outliers can make averages deceptive. Buenaventura reported cash costs up 64% year on year to $2,136.

Higher production means lower costs for ounce (other things being equal). Several companies raised their cost guidance, but we need to ask why. For some, this was simply because higher gold prices mean higher royalty payments.

An acquisition can see production decline over the total of the two companies (because of sales) also lower costs (because of synergies). We need to ask to what extent these changes were expected, and whether there could be additional production or cost declines.

Record Cash Flows Lead to Debt Reduction, Share Buybacks and Dividend Hikes

Not unexpectedly, margins increased again, 52% in the second quarter, and 78% year-of- year. The margin of $1,861 in the quarter was the highest ever, but follows two years of rapidly increasing margins, the most dramatic profit growth of any industry sector. It was only a matter of time before investors started to notice this.

For most companies, the second quarter has higher than normal taxes. That, and seasonal weather patterns, are why many companies typically have strong second halves. This year, most companies have been guiding to stronger 2Hs. We should look to see whether this held true in previous years. In addition, some companies have new mines ramping up, which should see improvements in production and costs as the year progresses.

Despite the strong cash flows over several quarters, producers continue to stay disciplined. They have increased share buybacks, last quarter $1.5 billion worth, up 174% from Q1; in addition, there have been many announcements of future large-scale buyback programs, notably from Newmont, which has approved a $3 billion program, as well as Kinross Gold Corp. (K:TSX; KGC:NYSE), and outside of gold form Altius Minerals Corp. (ALS:TSX).

Note: the announcement of a buyback program does not of course meant that the shares will actually be repurchased. In addition, dividends have increased. Several companies have base dividends with a variable component based on various criteria. Barrick boosted its dividend by 50%, with the bonus dependent on its net cash position. That does not mean that the higher rate will necessarily be paid in the future.

Above all else, however, companies paid down their debt, with several more companies going to a positive net cash position, including Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) and Barrick.

Many of the Top Post-Earnings Performers Have One Thing in Common

Best performers among the large and intermediate miners after earnings reports and analyst calls include Newmont, Equinox Gold Corp. (EQX:TSX; EQX:NYSE.A), Kinross, Barrick, Pan American Silver Corp. (PAAS:TSX; PAAS:NASDAQ), and Fortuna Mining Corp. (FSM:NYSE; FVI:TSX; FVI:BVL; F4S:FSE), as well as several of the royalty companies, led by Metalla Royalty & Streaming Ltd. (MTA:TSX.V; MTA:NYSE American), Royal Gold Inc. (RGLD:NASDAQ), and Franco-Nevada.

We hold a large number of these top performers on our “Current Positions” recommended list. In this discussion, we will exclude the royalty companies, which generally did very well and which we have discussed in detail before, and look at the miners to see why these outperformed. Although the reason is not the same for every company that outperformed, there are some broad themes, and one clearly is whether an underperforming company exceeded expectations.

Newmont Exceeded Soft Expectations

Newmont had underdelivered for years, and even the merger with Newcrest had not delivered great results, other than strong asset sales, and the stock reflected this underperformance. There was additional nervousness around the unexplained departure of the company’s Chief Financial Officer just a couple of weeks before the quarterly results. But contrary to fears, the CFO departure did not seem to reflect broader issues, and the quarter exceeded expectations, both on production and costs, with free cash flow of $1.7 billion against a consensus estimate of $733; that’s a beat! In addition, a massive share buyback program was announced.

Newmont went into earnings trading at a lower valuation that other majors (for example, 1.2 times p/npv vs 1.6x for AEM). The stock went from $62 to $74 in the month after. If the market believes Newmont can continue to execute, the stock could continue to do well. There is additional room to bring down costs after the merger to match those of its large-cap peers, including cutting its bloated workforce. However, unlike most companies, Newmont will have higher taxes in the second half, and its capex will increase. Though his has been flagged by the company, if it results in higher costs and lower cash flow in the third quarter, the market may react poorly.

Barrick Is Playing Catch up After Years of Misses

As we have discussed, Barrick Mining reported operating results largely in line with expectations, consistent with Barrick’s targets. It stepped up share buybacks, repurchasing $268 million in shares, and paid a 50% bonus on its dividend under its dividend policy. The company finished the quarter with a small net-cash positive position; at the end of the first quarter it had net debt of over $600 million. Barrick reiterated its full-year guidance. The company has been consistent in saying that production will increase each quarter, so the production guidance looks on track. In prior years, Barrick’s 2H has been regularly better than 1H, so there is no reason not to expect that this year.

The results were solid, and there is reason to be positive that the company has turned the corner. Barrick remains undervalued, particularly on an asset basis. Barrick long been underperforming, continually failing to meet optimistic targets. The stock was flat for more than a month before earnings, and, though it fell immediately after its earnings were released on the $1 billion write down for Mali, it recovered after the earnings call. If it can continue to execute, without another political problem hitting the company, the stock can continue to outperform.

Kinross had a modest production beat, with mixed results at different mines, but costs were lower than expected, with cash costs of $1,074. It continues an aggressive buy-back program and its guidance was maintained. Investors had been cautious given flawless performance and strong stock performance for the last 18 months, but continuing execution as well as its leverage to gold mean stock can continue to do well. It remains good value on cash flow.

Pan American Too Exceeded Expectations

As discussed, Pan American Silver reported an earnings beat on lower costs, setting new records on earnings and cash flow, this despite mixed production results (down 2% on the first quarter) amid grade reconciliation issues. However, free cash flow was up strongly and the company increased its dividend by 20% and repurchased $11 million in shares, as it reiterated its full-year guidance which is second-half weighted.

The second quarter was another sign that the major mine operational problems that afflicted the company in prior years were now behind it. It trades at an NAV discount to peers and continued execution will see the stock continue to outperform. In addition, any positive development on Escobal would be a catalyst for further stock price revaluation.

Fortuna: A Case Study in Market Misunderstanding

Fortuna Mining released second-quarter financials in line with expectations, with adjusted earnings were above analyst consensus. All mines are meeting expectations, and the company ended the quarter with $250 million net cash (and $537 million in available liquidity). Full-year guidance was maintained.

An apparent negative was the higher-than-expected All-in Sustaining Costs at $1,932, but this was due to increased capital costs at two mines which will result in increased production. Cash costs were a very reasonable $929.

Production, however, was down on the year-ago quarter, and this was completely because the company had sold two mines, both approaching their end of life. There were other factors making both sales actually positive for the company (see Bulletin #975), but most important for this discussion, these two mine sales had been well discussed by the company for months, and so the drop in production should clearly have been expected.

Output from continuing operations was up nicely.

But the headline production drop and AISC rise saw a massive 13% drop in the share price. This was perverse: the mine closures were known; the higher costs were for good and temporary reasons; and everything else about the results was positive.

The market soon realized its error; since the drop, Fortuna has been the best performing gold stock. (Even if one bought ahead of the earnings, and suffered a 13% drop right away, the stock is still up more than Agnico, matches Newmont, and almost matches Kinross.) There is a clear lesson here.

Equinox Shows What Can Happen When Expectations Are Low

Equinox Gold beat expectations, and is at an inflection point after a period of disappointing operational and financial results. A new CEO (from Calibre which merged with Equinox earlier in the year) he is well respected and has instilled much confidence after this first analyst call. A new COO has been appointed as well. Cashflows could rise significantly in the second half of the year and 2026, as Greenstone gets on the right track, while a new mine, Valentine (from Calibre) ramps up. Increased cash flow will see an improvement in the balance sheet (which had been another major concern).

As the issues that had plagued the company are being resolved, then the stock’s low valuation should improved. The market had long been wary given repeated misses, so it was primed to move. Since its (late) earnings release, it has been the top performer.

Different companies can be the top performer from the different dates of their earnings release and conference call, and often a stock will have its biggest move in the day or two after it releases. Of course companies that report after a string of other companies with strong results will tend to have higher expectations ahead of their earnings.

Underperformers That Exceed Expectations Can Be Top Performers

We can see some clear lessons here, however. A serial underperformer which has a strong quarter evidencing signs of a fundamental turnaround will rally strongly. So too will a company going into earnings with low expectations which outperforms (often the same). These stocks will often go into the earnings with subdued stock prices and low valuations, giving the opportunity to catch up. Best of all, however, is if a stock drops on a misunderstanding of their results, giving observant and nimble investors the opportunity for significant near-term outperformance.

As we look ahead, as discussed above, the gold price for the third quarter will likely be appreciably higher than it was in the second quarter, while costs will likely remain relatively stable. That along suggests another strong quarter. In addition, as discussed, the second half is generally stronger than the first half, both because of timing of tax payments and seasonal production patterns.

Record Increases in Free Cashflow Should Attract Attention

Yet another quarter of rising cash flows, following two years of dramatically increased cash flows, the highest growth for any industry sector, should see yet more investors start to take notice.

After the strong stock price appreciation this year, however, even though valuations remain attractive, investors are beginning to look away from the prior winners, the most solid stocks such as Agnico, and look for value or stocks that have lagged, as well as those that might exhibit more leverage. This can be dangerous, of course, since laggards often lag for good reason, while leverage comes with more risk.

But we are seeing a rotation into stocks like Barrick for a catch-up move, and a rotation from the large caps into the intermediate miners.

The bull market in gold equities still has much further to go.

Orogen’s Revenue up in Final Quarter Before Acquisition

Orogen Royalties Inc. (OGN:TSXV; OGNNF:OTC) reported financials for its second quarter, the final quarter before its acquisition and spin-out by Triple Flag. Royalty revenue was up 11% from the prior year, though flat quarter-on-quarter, but expenses rose 89% mostly due to the appreciation of the Canadian dollar, resulting in a net loss.

The quarter-end balance sheet is moot given the placement by Triple Flag and the large fees associated with the transaction. (See Bulletins #958 and 959).

Though royalty revenue was flat on the quarter, we look ahead to further growth at the Ermitaño deposit continues to expand with new discoveries.

The new Orogen is a Buy.

TOP BUYS this week include Nestle SA (NESN:VX; NSRGY:OTC), Nestle SA (NESN:VX; NSRGY:OTC), and Lara Exploration Ltd. (LRA:TSX.V).

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Barrick Mng Corp., Franco-Nevada Corp., Altius Minerals Corp., Agnico Eagle Mines Ltd., Equinox Gold Corp., Fortuna Mining Corp., Pan American Silver Corp., Metalla Royalty & Streaming, and Lara Exploration Ltd.

- Adrian Day: I, or members of my immediate household or family, own securities of: All. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: All. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Adrian Day Disclosures

Adrian Day’s Global Analyst is distributed for $990 per year by Investment Consultants International, Ltd., P.O. Box 6644, Annapolis, MD 21401. (410) 224-8885. www.AdrianDayGlobalAnalyst.com. Publisher: Adrian Day. Owner: Investment Consultants International, Ltd. Staff may have positions in securities discussed herein. Adrian Day is also President of Global Strategic Management (GSM), a registered investment advisor, and a separate company from this service. In his capacity as GSM president, Adrian Day may be buying or selling for clients securities recommended herein concurrently, before or after recommendations herein, and may be acting for clients in a manner contrary to recommendations herein. This is not a solicitation for GSM. Views herein are the editor’s opinion and not fact. All information is believed to be correct, but its accuracy cannot be guaranteed. The owner and editor are not responsible for errors and omissions. © 2023. Adrian Day’s Global Analyst. Information and advice herein are intended purely for the subscriber’s own account. Under no circumstances may any part of a Global Analyst e-mail be copied or distributed without prior written permission of the editor. Given the nature of this service, we will pursue any violations aggressively.

( Companies Mentioned: AEM:TSX; AEM:NYSE, ALS:TSX, ABX:TSX; B:NYSE, EQX:TSX; EQX:NYSE.A, FSM:NYSE; FVI:TSX; FVI:BVL; F4S:FSE, FNV:TSX; FNV:NYSE, K:TSX; KGC:NYSE, MTA:TSX.V; MTA:NYSE American, NEM:NYSE;NGT:TSX;NEM:ASX, NVDA:NASDAQ, OGN:TSXV;OGNNF:OTC, PAAS:TSX; PAAS:NASDAQ, RGLD:NASDAQ, )

Source: https://www.streetwisereports.com/article/2025/09/08/are-investors-returning-to-gold-stocks.html

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,734,004,527 |

| Stories: | 8,508,336 |

Whistler Blowers, Insiders