Global Stocks, US Futures Hit New Record Highs As Google Earnings Boost AI Theme

Global stocks extended their rally to fresh record highs on the prospect of more trade deals with the US, easing fears of a drawn-out tariff war while US equity futures are also higher led by Tech with small caps lower after yesterday’s outperformance, as sentiment was boosted by Alphabet signaling strong demand for its AI products, while Tesla posted the biggest revenue decline in at least a decade. As of 8:00am, S&P futures are 0.1% higher and Nasdaq futs gain 0.3% with the AI theme driving Tech following GOOG earnings with $10 billlion capex boost helping lift other AI infrastructure stocks in premarket trading, including NVDA and AVGO. Tesla slumped 6% after Elon Musk warned of difficult times ahead after losing electric vehicle incentives in the US. Cyclicals are stronger pre-market led by Industrials. Bond yields are 1bp from 2s to 30s with USD seeing its first bid in 5 sessions. Commodities are also higher led by Ags/Energy with weakness in both Base and Precious metals. Today’s macro data focus is on Flash PMIs, Jobless Claims, Home Sales, and regional Fed activity indicators.

In premarket trading, Mag 7 stocks were mostly higher: Alphabet (GOOGL) rose 3.6% after after the Google parent reported second-quarter results that beat expectations. Tesla (TSLA) fell 6% after Elon Musk warned of a hard year ahead for the electric-vehicle maker. Elsewhere, Nvidia +1.1%, Amazon +0.7%, Meta +0.02%, Microsoft -0.02%, Apple -0.1%). Here are the other notable premarket movers:

- American Airlines Group Inc. (AAL) falls 4% after the carrier reinstated its forecast this year, providing a wide range of possible outcomes.

- American Eagle (AEO) is up 16%, putting the stock on track to extend gains, after the apparel retailer announced a campaign headlined by actress Sydney Sweeney. Also, the stock was mentioned on the WallStreetBets page of Reddit, which has been known for sparking bouts of meme-stock activity.

- ASGN (ASGN) rises 8% after the IT services company reported second-quarter results that beat expectations.

- Blackstone Inc. (BX) rises 2% after reporting a 25% jump in distributable earnings for the second quarter, buoyed by profits from its retail and evergreen funds.

- Community Health Systems Inc. (CYH) sinks 29% after the owner and operator of hospitals cut the top end of its year forecast range for adjusted Ebitda and announced the retirement of CEO Tim Hingtgen.

- Dow (DOW) slumps 9% after the chemicals producer reported adjusted operating loss per share for the second quarter that missed estimates. The company also cut it’s quarterly dividend.

- International Business Machines (IBM) falls 6% after the IT services company reported second-quarter results that featured a disappointing read on its software business.

- Las Vegas Sands (LVS) climbs 6% after the casino and resorts operator reported adjusted earnings per share for the second quarter that beat the average analyst estimate.

- MaxLinear (MXL) soars 25% after the semiconductor device company reported second-quarter results that beat expectations and gave a forecast.

- Mobileye Global (MBLY) gains 4% after the maker of software and hardware technology for automobiles boosted its revenue forecast for the full year.

- ServiceNow (NOW) advances 6% after the software company reported second-quarter results that beat expectations and raised its full-year forecast for subscription revenue.

- T-Mobile (TMUS) gains 4% after the nation’s second largest wireless provider boosted its postpaid net customers guidance for the full year.

- Tractor Supply (TSCO) rises 3% after reporting comparable sales for the second quarter that beat the average analyst estimate.

- Viking Therapeutics (VKTX) drops 8% after the obesity drug developer reported second-quarter loss per share that was wider than the average analyst estimate.

- West Pharmaceutical Services (WST) gains 23% after the company boosted its adjusted earnings per share guidance for the full year.

As earnings season picks up pace, investors are keen for reassurance that the record-breaking US rally can continue and that lofty valuations are justified. Europe’s stocks climbed following reports the US is closing in on an agreement with the European Union to set a 15% tariff for most products.

“We still see some companies being able, especially in the US, to deliver very strong results and so probably valuations are less questionable now,” Claudia Panseri, chief investment officer for France at UBS Wealth Management, told Bloomberg TV. “People were expecting a lot of downside.”

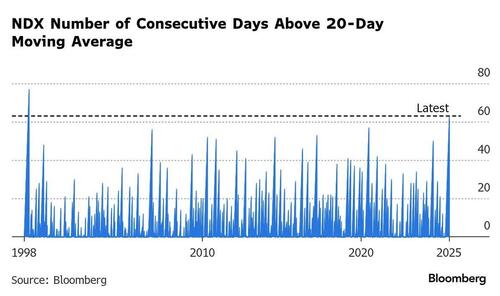

The Nasdaq posted its 63rd consecutive day above its 20-day moving average, the longest streak since 1999, suggesting investors are all-in on tech. Still, things have calmed down a bit on the meme stock front, with only Opendoor particularly active premarket.

As an Aug. 1 deadline on US trade tariffs nears, traders are watching the latest news on talks with countries around the world. Trump has suggested he won’t go below a rate of 15% as he sets so-called reciprocal tariff rates ahead of the cutoff date. Delegations from the US and China are also due to hold negotiations in Stockholm next week for their third round of trade talks. Meanwhile, the US and South Korea have discussed creating a fund to invest in American projects as part of a trade pact, similar to an agreement Japan struck Tuesday.

In Europe, the Stoxx 600 index was trading up 0.4% buoyed by upbeat earnings and reports that US and EU are near a deal to set a 15% tariff on most products. On one of the busiest days in the earnings season in Europe, Deutsche Bank shares jumped to the highest in a decade after the lender reported strong trading results. Meanwhile, BNP Paribas SA rose 3% after posting a better-than forecast profit. Luxury firm LVMH is due to report after the close. Telecoms, personal care and banks are the strongest-performing sectors. Later Thursday, the European Central Bank is set to leave interest rates untouched for the first time in more than a year as it awaits clarity on the impact of President Donald Trump’s trade levies on inflation. Data showed the euro area’s private sector grew at the quickest pace since last August. Here are the biggest movers Thursday:

- Neste surges as much as 18%, the most since 2022, after the Finnish oil and renewables firm reported earnings and reiterated its 2025 outlook

- Howden Joinery Group shares jump as much as 11%, most since 2020, after the kitchen supplier’s revenue and profits grew more-than-expected in the first half

- Reckitt Benckiser shares soar as much as 11% to trade at their highest level since February 2024 after the consumer goods company raised its organic growth outlook for the full year

- ITV shares jump as much as 9.7%, the most intraday since November, after the broadcaster reported profits well ahead of estimates in the first half

- BE Semiconductor shares climb as much as 8.5% after the chip-tool maker said that the second-half outlook improved in recent weeks based on customer feedback

- Bankinter shares advanced as much as 7.4% to hit a record high after the Spanish lender reported net income for the second quarter that beat estimates, with a strong lending revenue beat

- Aalberts slumps as much as 14% after the industrial technology company said the first half of year has been characterized by continued softness in end markets

- SEB SA falls as much as 16%, the most since 2018, after the French home appliances manufacturer cut its full-year forecast, while its first-half results significantly missed estimates

- Eurazeo falls as much as 12%, the most since March 2020, after posting a bigger net loss in the first half than a year ago. Degroof Petercam cuts its recommendation to reduce from hold to reflect a significant slowdown in growth

- Nestle shares fall as much 5.1% after the world’s largest food company reported weaker-than-expected volumes in the second quarter, weighed down by disappointments in China and the health science division

Earlier in the session, Asian stocks also added to their strong gains from Wednesday as investors bet that progress in trade deals will help clear the uncertainty that’s clouded the economic outlook for months. The MSCI Asia Pacific Index rose as much as 1.1%, with cyclical sectors — industrials and financials — leading gains. Chip and tech-related shares also climbed after Alphabet reported strong second-quarter revenue growth and raised its 2025 capital expenditure plan, and South Korea’s SK Hynix outlined plans to speed up spending on advanced memory chip production capacity after reporting record earnings. Japanese stocks once again led gains in the region, extending Wednesday’s rally sparked by the announcement of a trade deal that set a 15% levy on Japanese exports to the US. The Topix climbed to an all-time high. The MSCI Asia gauge rose more than 2% on Wednesday to reach its highest close since June 2021. The regional benchmark is on course for a sixth straight day of gains, which would mark its longest winning streak since January. A gauge of global equities is at a record. Here are the most notable Asian movers:

- Dr Reddy’s shares gain as investors focus on growth prospects of the drugmaker as it plans fresh investments and launches, despite reporting June-quarter earnings that were below estimates.

- Persistent Systems’ shares fall as much as 9.3%, the most since April 7, after the Indian IT firm reported 1Q results that Citigroup described as “soft”.

- Indian Energy Exchange’s shares drop by the 20% lower limit, the most since March 2020, after the country’s power regulator ordered the coupling of the nation’s day-ahead power markets starting Jan. 2026 to homogenize price discovery at power exchanges.

- Infosys Ltd.’s shares slipped in early Mumbai trading after the software exporter’s June quarter earnings failed to quell concern about the outlook for spending by big businesses at a time of weakening demand. The shares declined as much as 1.4% and are down roughly 17% for the year.

- Zhongjin Gold shares decline as much as 8.1% in Shanghai, after the Chinese company said six university students drowned and one teacher was injured at its unit’s mine during a July 23 visit.

- WuXi Biologics shares rise as much as 2.1% in HK after the co. said it expects profit attributable to equity shareholders for the six months ended June 30 to increase 56% from a year earlier.

In FX, the pound fell to a session low versus the dollar, underperforming G-10 peers, after PMIs showed the economy struggled to grow. The Bloomberg dollar spot index rose 0.1%, pulling the euro 0.2% down ahead of the ECB meeting later. The central bank is expected to hold rates steady for the first time in over a year as policymakers assess the fallout from Trump’s trade policies. Separately, Thailand’s baht fell from the strongest level in more than three years after the government said Thai fighter jets attacked two Cambodian army posts.

In rates, yields are near session highs with the 10-year higher by more than 2bp at about 4.40%, near its 50-day average level which it’s been below since Monday. Gilts outperformed peers across the curve. The UK 10-year yield fell one basis point, while comparable Treasury yields climbed a basis point, and the German 10-year rates rose 2.5bps. Treasury sells $21 billion 10-year TIPS new issue at 1pm; auction faces an array of challenges ranging from its record size to weaker-than-expected demand for most of the six annual auctions of the tenor over the past two years

In commodities, Brent rose 1.1% near $69.25. Most base metals traded in the green. Spot gold fell roughly $23 to trade near $3,365/oz.

Looking to the day ahead now, the main highlight will be the ECB’s latest policy decision, along with President Lagarde’s subsequent press conference. Otherwise, data releases include weekly initial jobless claims, and new home sales for June. Earnings releases include Intel.

Market Snapshot

- S&P 500 mini little changed, Nasdaq 100 mini +0.3%

- Russell 2000 mini -0.3%

- Stoxx Europe 600 +0.5%

- DAX +0.8%, CAC 40 +0.1%

- 10-year Treasury yield +1 basis point at 4.39%

- VIX -0.1 points at 15.3

- Bloomberg Dollar Index little changed at 1194.15

- euro -0.1% at $1.1754

- WTI crude +1.2% at $66.05/barrel

Top Overnight News

- Trump will personally participate in a tour of the Fed headquarters on Thurs as the White House ratchets up pressure on Powell to lower rates. FT

- Trump signed AI executive orders to fast-track big projects and to turn America into an AI export powerhouse: RTRS.

- White House official told Reuters on Wednesday that the administration was not denying that President Trump’s name appears in the files.

- US Treasury Secretary Bessent a new Fed Chairman nominee is likely to be announced in December or January.

- US trading partners will face tariffs ranging from 15% to 50%, Trump said, as he sets rates ahead of an Aug. 1 deadline. BBG

- The US and South Korea have discussed creating a fund to invest in American projects as part of a trade deal, similar to an agreement Japan struck Tuesday with President Donald Trump. BBG

- TSLA -6% pre mkt, after Musk shared that Tesla could be in for a “rough few quarters” on call as the Trump administration ends EV incentives and tariff pressures cause uncertainty for the company following one of its worst earnings reports in 10+ yrs. BBG

- The ECB is in wait-and-see mode with no change to rates or language expected at today’s meeting. Instead, Bloomberg Economics sees a 25-bp cut in September to cushion the impact of the US tariffs. BBG

- China’s investment banks have slashes fees for bond issues to as low as $100 as price-sensitive state-owned issuers dominate a tepid credit market and stoke a race to the bottom to win mandates. Bankers aid the pressure to undercut rivals had become acute this year as state owned enterprises had become the most active bond issuers and private companies pulled back. FT

- Japan’s flash PMIs for Jul are mixed, with manufacturing coming in at 48.8 (down from 50.1 in June) and services at 53.5 (up from 51.7 in June). BBG

- Eurozone flash PMIs for Jul are a bit better than expected thanks to strength in services (51.2, up from 50.5 in June and above the Street’s 50.6 forecast) while manufacturing was inline (49.8, up from 49.5 in June and inline w/the Street’s 49.8 forecast), and the report contained some glimmers of hope on the inflation front as price pressures eased somewhat. S&P

- BofA Institute Total Card Spending (w/e July 19th): +1.8% Y/Y (vs. +0.2% June avg.); despite base effect from Prime Day (AMZN) timing change, spending growth was solid.

Trade/Tariffs

- EU diplomats say that members have supported potential tariffs on EUR 93bln of US goods

- US President Trump said they will have straight, simple tariffs of between 15% and 50% on countries, while he added the US is in serious talks with the EU and if they agree to open up to US businesses, US will let them pay lower tariffs. Trump said they will be charging straight tariffs to most of the rest of the world and are in the process of completing a deal with China, while they are making deals with various Asian countries on energy and made a deal with the EU but it was related to military equipment.

- White House said on reports of an EU trade deal, that discussions about a possible deal should be considered speculation.

- South Korea’s Finance Ministry said the 2 + 2 trade talks with the US were cancelled due to the US Treasury Secretary’s schedule, while the US proposed talks in the immediate future and the sides will set the time for another round of talks ASAP. Furthermore, it stated that South Korea’s trade envoy is to still meet with his US counterpart during his trip, while there were separate reports that the US and South Korea have discussed creating a fund to invest in American projects as part of a trade deal and South Korea is to invest more than USD 100bln as part of a US trade deal, according to Yonhap.

- Japan’s Tariff negotiator Akazawa says there is no difference in understanding between Japan and the US on the trade deal; had no discussion with US President or US officials on how to implement the deal.

- Indonesia Chief Economy Minister says its possible that Indonesia’s key commodities could get a lower tariff than 19% or even close to 0%.

- Indonesian Economy Minister says Indonesia has asked the US for lower tariffs on goods produced in the free trade zone.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly extended on gains following the positive handover from Wall St and as recent trade developments continued to underpin risk sentiment. ASX 200 lacked conviction and lagged behind regional peers with heavy losses seen in gold miners after a drop in the precious metal, while participants also digested several quarterly production updates. Nikkei 225 continued its rally and briefly breached the 42,000 level to the upside as the euphoria from the US-Japan trade agreement lingered and with the electrical equipment manufacturers leading the advances, although the index has since pulled back from today’s best levels. Hang Seng and Shanghai Comp were higher with little fresh catalysts to derail the recent positive momentum and following some optimistic comments from US Treasury Secretary Bessent ahead of next week’s US-China talks in Sweden in which he stated that they are in a very good place with China right now and are back on track with China negotiations, while he also seemingly suggested they could do a rolling 90-day deadline when asked about the tariff deadline with China.

Top Asian News

- Chinese President Xi said China and the EU are at another critical historic juncture and should enhance communication, increase mutual trust and deepen cooperation, while China and EU leaders should demonstrate vision and responsibility, as well as make correct strategic choices that meet the expectations of the people.

- EU’s von der Leyen said rebalancing bilateral relations is essential and they have reached an inflection point, while she added it is vital for China and Europe to acknowledge respective concerns and come forward with real solutions. President von der Leyen said as cooperation has deepened, so have imbalances and noted that the China–EU relationship is one of the most important and consequential in the world.

- European Council President Costa said to Chinese President Xi that they need concrete progress on issues related to trade and the economy.

- US Commerce Secretary Lutnick said regarding the TikTok sale that he thinks a deal will happen and America will buy it.

- US lawmakers subpoenaed JPMorgan (JPM) and Bank of America (BAC) over the IPO of a Chinese battery startup, while the House committee had previously urged banks to stop work on CATL’s initial public offering, according to WSJ.

- PBoC Statement: China to support stable development of industries such as hogs, beef cattle, dairy cattle, sheep, and aquatic products.

European bourses (STOXX 600 +0.5%) opened stronger across the board, with positive trade developments continuing to boost sentiment. However, as the morning progressed, indices have dipped off earlier highs but still reside firmer across the board. Sentiment boosted today thanks to an FT report which suggested that the US and the EU were closing in on a trade deal with a 15% tariff rate, albeit this is yet to be officially confirmed. European sectors hold a strong positive bias, with the industry compilation today largely dictated by post-earning movers. Optimised Personal Care tops the pile, largely driven by Reckitt which soars after the Co. reported a Q2 sales beat, lifted its annual guidance and plans a GBP 1bln share buyback. Banks take second spot, lifted by post-earning strength in Deutsche Bank and BNP Paribas. Food Beverage and Tobacco underperforms alongside Real Estate today; the former has been pressured by heavyweight Nestle, after its results. (details all below).

Top European News

- EU HCOB Composite Flash PMI (Jul) 51.0 vs. Exp. 50.8 (Prev. 50.6); Manufacturing Flash PMI (Jul) 49.8 vs. Exp. 49.7 (Prev. 49.5); Services Flash PMI (Jul) 51.2 vs. Exp. 50.7 (Prev. 50.5)

- French HCOB Composite Flash PMI (Jul) 49.6 vs. Exp. 49.3 (Prev. 49.2); French HCOB Services Flash PMI (Jul) 49.7 vs. Exp. 49.6 (Prev. 49.6); HCOB Manufacturing Flash PMI (Jul) 48.4 vs. Exp. 48.5 (Prev. 48.1)

- German HCOB Services Flash PMI (Jul) 50.1 vs. Exp. 50.0 (Prev. 49.7); HCOB Manufacturing Flash PMI (Jul) 49.2 vs. Exp. 49.5 (Prev. 49.0); Composite Flash PMI (Jul) 50.3 vs. Exp. 50.7 (Prev. 50.4)

- UK Flash Services PMI (Jul) 51.2 vs. Exp. 53.0 (Prev. 52.8); Flash Composite PMI (Jul) 51.0 vs. Exp. 51.8 (Prev. 52.0); Manufacturing PMI (Jul) 48.2 vs. Exp. 48.0 (Prev. 47.7)

FX

- DXY is a touch higher after a run of four consecutive daily losses. Yesterday’s downside was largely due to the appreciation of the JPY in the wake of the US-Japan trade deal. ING has made the observation that “The dollar didn’t suffer in the first half of July from trade tensions re-escalating. And it is equally finding no benefit from positive trade deal news”. Noise around the Trump administration’s disdain for the current direction of FOMC policy will likely pick up today with the President set to visit the Fed at 21:00BST. DXY has delved as low as 97.10 with focus on a test of 97.00; not breached since 7th July (96.89 was the low that day).

- EUR is a touch softer vs. the USD with the recent rally pausing for breath. This week has seen optimism increase on the trade front with reporting via Reuters and the FT suggesting that the US and EU are closing in on a 15% tariff deal, which would waive tariffs on some products. Elsewhere, flash EZ PMI metrics for July showed minor improvements and beats on expectations for the manufacturing, services and composite metrics. The accompanying report said the data was indicative of “robust” economic growth for Q3 and a continuation of the disinflation trend. That being said, the release is unlikely to have any sway on the upcoming ECB rate decision with markets fully priced for an unchanged rate as the GC views current policy as well-positioned.

- JPY is mildly extending on its recent run of gains vs. the USD with the Yen buoyed after securing a trade deal with the US, which will see Japanese goods subject to a 15% tariff (including autos). Additionally, Japan will invest USD 550bln into the US and is expected to sign an LNG deal with the US. Accordingly, markets have continued to bolster bets on BoJ tightening this year with 22bps of hikes seen by year-end vs. circa 14bps at the start of the week. USD/JPY has briefly made its way onto a 145 handle with a session low at 145.86; lowest since July 10th.

- GBP is struggling and sits at the bottom of the G10 leaderboard in the wake of disappointing flash PMI metrics for July. The services metric unexpectedly declined to 51.2 from 52.8, manufacturing nudged higher to 48.2 from 47.7 with the composite coming in at 51.0 vs. previous 52.0. The accompanying release was a gloomy one with S&P Global noting the data showed “output growth weakened to a pace indicative of the economy growing at a mere 0.1% quarterly rate, with risks tilted to the downside in the coming months”. Cable has slipped to a low of 1.3547 but is holding above its 50DMA at 1.3529 and yesterday’s low at 1.3515.

- Antipodeans both remain buoyed by the encouraging risk tone in the absence of any antipodean-specific drivers. As such, both will likely take direction from the trade environment in the short-term.

- PBoC set USD/CNY mid-point at 7.1385 vs exp. 7.1503 (Prev. 7.1414).

Fixed Income

- Bunds are under pressure into the ECB. Weighed on by the constructive updates on the EU-US trade front. As reports noted that the US and the EU were closing in on a trade deal with a 15% tariff rate, albeit this is yet to be officially confirmed, and White House Trade Adviser Navarro said to take it with a pinch of salt. Bunds find themselves lower by 87 ticks at most to a 129.71 base, notching a marginal new WTD trough. As for PMIs, the French and German figures were mixed vs consensus while the EZ figure beat and came in above the prior for all metrics. Attention now turns to the ECB, where rates are expected to be kept steady.

- USTs are also in the red, but to a much lesser extent. Directionally in-fitting with EGBs but holding around the 111-00 mark after a brief blip to a 110-28+ low in the European morning. In contrast to Bunds, the current low is clear of Monday’s 110-24 WTD base. Trade aside, the Fed remains in focus as Trump himself will be visiting the Fed this evening. Currently, it is unclear if he will be meeting with Chair Powell or not during this visit. Docket ahead will include US Jobless Claims, PMIs and the US 2, 5, 7, 2yr FRN Refunding Announcement.

- Gilts opened lower by 26 ticks given the risk tone and pressure in Bunds at the time. Thereafter, it extended to a 92.29 trough ahead of its own PMI data. Metrics which were mixed vs expectations but featured a sizeable miss in Services at 51.2 (exp. 53, prev. 52.8) coming in outside of the forecast range. Internal commentary was also downbeat, S&P calculating output growth is indicative of just 0.1% quarterly growth and risks are tilted to the downside in the coming months. In reaction to the series, a move higher from 91.43 to a 91.57 peak occurred just after the series, given the mixed/weak headlines.

- Italy sells EUR 2.75bln vs exp. EUR 2.25-2.75bln 2.10% 2027 BTP & EUR 1.5bln vs exp. EUR 1.25-1.5bln 1.10% 2031 I/L.

Commodities

- Firmer trade across the crude complex with a bulk of this morning’s price action commencing just before 07:00 BST as European traders entered the fray, to the trade optimism felt across markets following the US-Japan deals alongside unofficial reports of an EU-US deal, although US officials suggested taking these reports with a pinch of salt. The price action also coincided with commentary from US envoy Barrack, who said Lebanon’s failure to disarm Hezbollah means that the Israeli raids will continue. WTI resides closer to the upper end of a USD 65.37-66.24/bbl range, while Brent sits in a USD 68.61-69.45/bbl range.

- Precious metals are lower across the board amid the outflow of havens on trade optimism, with a similar performance seen across the bond market. Spot gold resides in a USD 3,366-3,393.48/oz range at the time of writing.

- Base metals are flat/mixed despite the broader risk appetite as traders gear up for trade deals ahead of next Friday’s deadline, with the EU and US on watch, whilst officials from Washington and Beijing also gear up for a meeting next week, in Sweden. Furthermore, markets are also on the lookout for details regarding the US copper tariff. 3M LME copper resides in a USD 9,923.05-9,969.00/t range.

- China June YTD gold output fell 0.3% Y/Y to 179.083 metric tons and China June YTD gold consumption fell 3.54% Y/Y to 505 metric tons. according to the China Gold Association.

Geopolitics

- North Korea leader Kim supervises artillery firing, according to KCNA

- US Envoy Barrack says Lebanon’s failure to disarm Hezbollah means that the Israeli raids will continue; ” There is no open deadline for disarming Hezbollah and the one who decides the duration of this period is Israel, not the United States”. Elsewhere, “The likelihood that Iran will not conclude a deal with the United States is “very small”, according to Sky News Arabia.

- Israeli officials say “At present, it is not possible to determine whether Hamas new response is indeed improved or allows for progress. Consultations will be held in the coming hours.”, via Jerusalem Post’s Stein; follows, PM Netanyahu says they are examining the Hamas response to the Gaza ceasefire proposal.

- Russia’s Kremlin says did not expect a breakthrough from talks with Ukraine, according to Tass.

- Russia’s Kremlin says it is hard to see how President Putin and Ukrainian President Zelensky could meet before the end of August.

- Thailand acting PM says Cambodia has fired heavy weapons into Thailand without specific targets, civilians have been killed; there has been no declaration of war; conflict has not spread to more provinces.

US Event Calendar

- 5:00 am: Jun F Building Permits, est. 1397k, prior 1397k

- 8:30 am: Jul 19 Initial Jobless Claims, est. 226k, prior 221k

- 8:30 am: Jun Chicago Fed Nat Activity Index, est. -0.15, prior -0.28

- 8:30 am: Jul 12 Continuing Claims, est. 1953.5k, prior 1956k

- 9:45 am: Jul P S&P Global U.S. Manufacturing PMI, est. 52.7, prior 52.9

- 9:45 am: Jul P S&P Global U.S. Services PMI, est. 53, prior 52.9

- 9:45 am: Jul P S&P Global U.S. Composite PMI, est. 52.8, prior 52.9

- 10:00 am: Jun New Home Sales, est. 650k, prior 623k

- 10:00 am: Jun New Home Sales MoM, est. 4.33%, prior -13.7%

DB’s Jim Reid concludes the overnight wrap

The risk-on tone has continued over the last 24 hours, with the S&P 500 (+0.78%) at a fresh record thanks to growing optimism that more trade deals would be reached before August 1. The initial catalyst was the US-Japan deal we woke up to this time yesterday, with both European and US risk assets rallying as they caught up to the news. But around the time that European markets were going home, an FT headline said that the EU and the US were closing in on a similar deal that would also put 15% tariffs in place. So that would be the same rate as the Japan deal, and only half the 30% rate that Trump had threatened in his previous letter. Indeed, if a 15% total rate inclusive of existing tariffs is agreed as suggested, this would mark only a marginal increase compared to the 10% additional tariffs that EU exports to the US have faced since Liberation Day but with certainty about the future.

This optimism was clear on several fronts yesterday, and aside from the press reports, the noises from the negotiators were sounding much more positive. For instance, Treasury Secretary Bessent had said earlier that “We are making good progress with the EU.” Later on, Trump said the US is in “serious negotiations” with the EU and that ““we will let them pay a lower tariff” if the EU opens up to American businesses. Meanwhile on China, Bessent said that “we’re in a very good place with China” ahead of the two sides meeting next week. And on the 90-day tariff reduction that expires on August 12, he said “I think that we could roll it forward, maybe in a 90-day increment.” So when it comes to the major economies, there’s now a deal with Japan, headlines pointing to one with the EU, and Bessent signalling a roll-over of the tariff reduction with China. And Trump announced a deal with Indonesia as well yesterday.

All this created a very strong backdrop, and European equities rallied in particular as hopes for a deal mounted. Equity markets there closed just before the FT headline on the trade deal came through, but even before that news, the STOXX 600 (+1.08%) had already recovered after three days of losses. And notably, the STOXX Automobiles and Parts index (+3.76%) surged following the news that Japan had managed to get a lower tariff on automobiles. Euro futures are climbing this morning with the STOXX 50 and DAX futures trading +1.19% and +1.18% higher respectively.

US equities also had a strong day thanks to the trade headlines, with the S&P 500 (+0.78%) up to a fresh record. But whilst it was trade that drove the gains, after the close we then heard from Tesla and Alphabet, who are the first of the Mag 7 to report this quarter. Alphabet’s shares gained in after-hours trading as the company delivered a decent revenue beat, which it said was boosted by demand for AI products. The search giant also boosted its 2025 capex plan from $75bn to $85bn to meet AI-related cloud demand. This spending increase initially worried investors and shared dipped after the results but ultimately bounced back in the after hours trading period.

By contrast, Tesla’s shares fell by -4.4% post-market as the company missed revenue and profit estimates, with Q2 sales falling -12% year-on-year and CEO Musk warning of a few “rough quarters” ahead. Next week we’ve got four more of the Mag 7 announcing, including Meta and Microsoft on Wednesday, and then Apple and Amazon on Thursday.

Whilst equities were rallying, sovereign bonds put in a weaker performance given the risk-on tone. For example, Treasury yields moved higher across the curve, with the 2yr yield up +4.7bps to 3.88%, whilst the 10yr yield was up +3.7bps to 4.38%. The losses for Treasuries largely held despite a solid $13bn 20yr auction. We also had a fresh bout of criticism at Fed Chair Powell from President Trump, who said that “Housing in our Country is lagging because Jerome “Too Late” Powell refuses to lower Interest Rates.” He also called for rates to be “three points lower”, so that kept up the drumbeat of pressure from the administration, although markets have mostly taken out the extra risk premium they assigned to Powell’s removal last week. Trump is visiting the Fed today at 4pm local time so there’s possibilities for extra headlines from that visit.

Related to the central bank theme, Peter Sidorov yesterday published a note (link here) looking at key themes in global monetary and credit conditions, and his key takeaway for the US economy is that while its rate-sensitive sectors such as housing are lagging, aggregate US credit conditions are consistent with a Fed stance that is only modestly restrictive. See his report for more, including on the credit cycles in Europe and China.

Meanwhile in Europe, sovereign bonds did see a very late turnaround, as the FT headline on the US-EU trade deal came out in the brief period between the equity and the bond close. So that saw yields immediately move 3-4bps higher across the board, particularly as investors viewed the news as hawkish from the ECB’s standpoint. Indeed, the probability on another ECB rate cut by the September meeting came down from 51% the previous day to only 40% by the close last night. So that pushed yields higher, and those on 10yr bunds (+4.9bps), OATs (+3.6bps) and BTPs (+2.8bps) all moved up on the day after being relatively flat before the headlines.

Across other asset classes, the risk-on tone saw gold retreat by -1.29% from Tuesday’s record high, while the dollar index (-0.18%) lost ground for a fourth consecutive day.

Looking forward, the focus will be on the ECB today, with their latest policy decision at 13:15 London time. They’re widely expected to pause the current cycle of rate cuts, which would be the first decision to hold rates since their July 2024 meeting. However, markets don’t think they’re done cutting yet and, as our European economists note, the bigger question is whether this is a short pause until the subsequent meeting in September, or whether this is the start of a longer period on hold. Their view is that the ECB will want to leave their options open and have no incentive to make significant changes to their messaging this time. After all, uncertainty remains high, particularly around the August 1 tariff deadline and any potential retaliation by the EU. Yesterday’s news will perhaps help crystalise the ECB’s thinking a bit more but until a deal is confirmed they are unlikely to factor anything in. See here for our economists’ full preview. Also watch out for the flash European PMIs this morning for trends ultimately influencing the ECB.

Overnight in Asia, the MSCI Asia-Pacific index has been trading higher for the sixth consecutive day, marking its longest streak since January. Specifically, Japanese markets are approaching record highs, with the Nikkei rising by +1.53% and the Topix increasing by +1.62%, both benefiting from sustained optimism regarding a US trade agreement. Elsewhere, the Hang Seng has increased by +0.59%, the Shanghai Composite by +0.48%, and the KOSPI by +0.26%. S&P 500 (+0.11%) and NASDAQ 100 futures (+0.30%) are being helped by Google and 10yr USTs are up just over a basis point.

Overnight the S&P Global Japan services PMI rose to 53.5 in July from 51.7 in June, driven by growth in new business. Conversely, the manufacturing PMI fell to 48.8 in July from June’s final reading of 50.1, that had marked the first time in 13 months that the index had exceeded 50.0. This month’s fall obviously covered the period before the trade deal was announced. When combining both service and manufacturing activities, the composite PMI remained steady at 51.5, indicating four consecutive months of expansion.

Turning to Australia, S&P Global reported that the composite PMI increased to 53.6 in July, up from 51.6 previously, reaching its highest level since April 2022 and marking the tenth consecutive month of expansion. Furthermore, the services PMI rose to 53.8 in July from the previous reading of 51.8, achieving its fastest growth rate in 16 months. Meanwhile, the manufacturing PMI registered at 51.6 in July compared to 50.6 previously. New orders for manufactured goods have rebounded, resulting in the strongest overall growth in new business in over three years.

In FX, the Japanese yen (+0.30%) is gaining ground for the fourth consecutive session trading at 146.07 against the dollar on speculation that the Japan-US trade agreement has made it easier for the BOJ to raise interest rates.

Finally, there wasn’t much economic data yesterday, although US existing home sales fell a bit more than expected in June, down to an annualised rate of 3.93m (vs. 4m expected), which was their lowest in 9 months. Separately, the European Commission’s preliminary consumer confidence indicator ticked up to a 4-month high of -14.7 in the Euro Area (vs. -15.0 expected).

To the day ahead now, and the main highlight will be the ECB’s latest policy decision, along with President Lagarde’s subsequent press conference. Otherwise, data releases include the July flash PMIs from the US and Europe, the US weekly initial jobless claims, and new home sales for June. Earnings releases include Intel.

Tyler Durden Thu, 07/24/2025 – 08:21

Source: https://freedombunker.com/2025/07/24/global-stocks-us-futures-hit-new-record-highs-as-google-earnings-boost-ai-theme/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,721,276,081 |

| Stories: | 8,480,126 |

Whistler Blowers, Insiders