The Hormuz Hype: How Europe Got Played at the Oil Casino

Freddie Ponton

21st Century Wire

Europe’s oil shock was sold as a tragic consequence of the war on Iran and chaos in the Strait of Hormuz. The story was simple. Blame Tehran, blame geography, tell Europeans there was no choice but to pay. Yet official documents quietly admit that the EU’s direct dependence on Hormuz is limited and that the real impact came through prices, not empty fuel tanks.

While leaders repeated the script, Saudi crude was being rerouted around the strait through the East–West pipeline to Yanbu, Iraqi and Kazakh flows to Europe were kept alive through alternative corridors, and oil majors were telling investors that higher prices would boost profits. At the same time, on‑chain data shows a Hyperliquid whale at address 0x985f moving millions in stablecoins to build massive leveraged shorts on crude and Brent, turning the crisis into a 24‑hour casino. This investigation pulls those strands together and names what the official narrative left out. Europe did not just suffer a wartime oil shortage. It lived through a man‑made price storm in which benchmarks, trading houses, whales and regulators each played a part.

War on Iran: the perfect cover story

In March 2026, European leaders put the war on Iran at the centre of an energy drama that seemed to leave them powerless. Night after night, the public heard the same script. Iran had shut the Strait of Hormuz. One-fifth of the world’s oil usually passes through that narrow channel. Prices at the pump would inevitably explode. Any attempt to resist the shock, they implied, would be irresponsible or even impossible.

IMAGE: March 2026 EU leaders’ summit in Brussels, where the Hormuz “weaponisation” narrative was front and centre.

The French outlet France Soir was among the first to question whether this story really held up, asking whether the spike reflected genuine shortages or financial speculation. Their investigation raised the right question, but did not yet have the route‑level data or on‑chain evidence now available in our report.

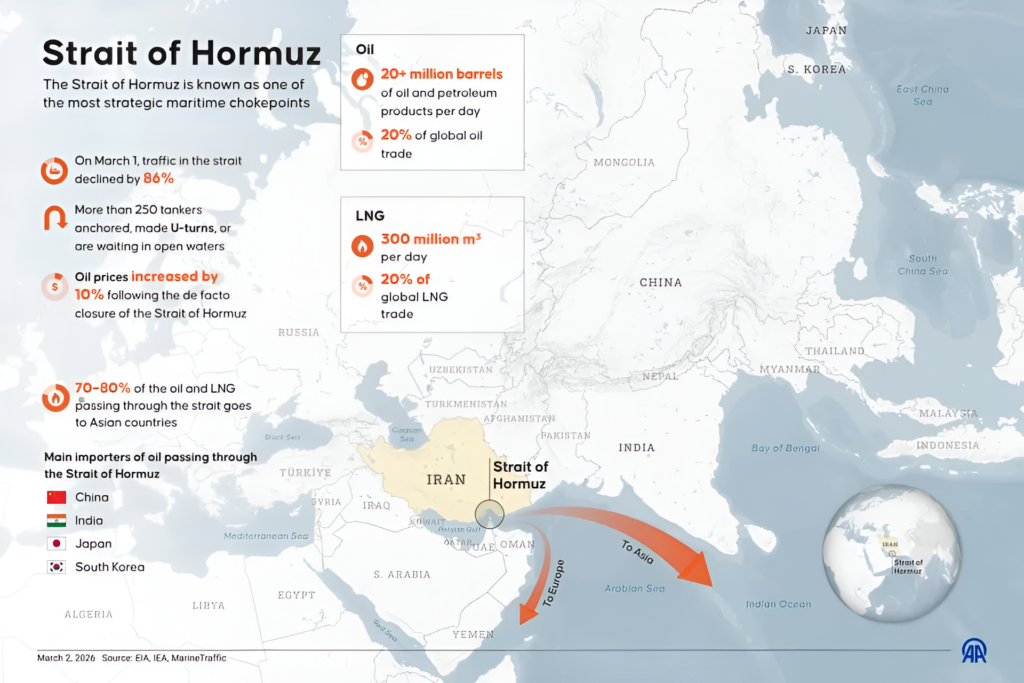

At their March summit in Brussels, EU leaders warned of the “weaponisation” of the strait and talked about only “temporary and targeted” responses to soaring energy costs. Yet in its own briefing on the Outcome of the meetings of EU leaders, 19 March 2026, the European Parliament quietly admitted that Europe’s exposure to Hormuz was actually limited and that the strait was hitting the bloc mainly through prices, not through direct physical dependence.

“[..] less than 7 % of the EU’s crude oil imports transit through the Strait” (Europarl)

That caveat never made it into the public talking points. Citizens were told a simpler story. Iran had turned off the tap. Europe had no choice but to pay. It sounded convincing because it wrapped a complex market in the language of war and sacrifice. It also hid the fact that Europe had spent a decade building a system in which a paper benchmark price in London or New York dictates what a family in Lyon or Leipzig pays for fuel.

Europe’s oil reality looked very different

Start with a basic question. Whose oil does Europe actually burn? The answer is not Iran. In a 2025 note on EU imports of crude oil, the European Parliament’s think‑tank shows the United States as the EU’s largest crude supplier at around 18 per cent of imports in recent quarters, with Norway at roughly 14 per cent and Kazakhstan near 8 per cent. Libya, Nigeria, Saudi Arabia and Iraq make up a large share of the rest. Iran barely registers.

IMAGE: Hormuz and Gulf route map showing that traffic could be rerouted (Source: Mehmet Yaren Bozgun—Anadolu/Getty Images)

That is not an accident. Back in 2012, the Council of the EU adopted sanctions that effectively shut Iranian crude out of the European market, terminating contracts and banning European insurers from covering shipments. Those measures are set out in the Council’s own notice on the Iran oil embargo exemptions, which end on 1 July 2012. Europe did not suddenly discover its dependence on Iranian oil in 2026. It had already chosen to walk away from those barrels years earlier.

Even inside the Gulf, the routes do not match the fear‑mongering. In late March, Reuters reported that Saudi crude exports from Yanbu were approaching capacity as the kingdom pushed crude through its East–West pipeline to the Red Sea, explicitly to bypass Hormuz during the war. A companion dispatch noted that the Saudi pipeline, pumping 7 million bpd of oil and bypassing Hormuz, gave Riyadh room to ship several million barrels a day clear of the strait.

IMAGE The East–West Crude Oil Pipeline, also known as the Petroline, across the width of the Arabian Peninsula to Yanbu at the Red Sea (Source: IEA)

To the north, Baghdad and Erbil struck a deal to restart Kirkuk crude exports via Ceyhan in mid‑March, sending flows from northern Iraq back toward Turkey’s Mediterranean coast. The pipeline’s long‑term capabilities are described in more detail by the Kirkuk–Ceyhan Oil Pipeline entry on Global Energy Monitor, which notes a design capacity well above the initial restart volume.

Further east, Kazakhstan continued to send most of its exports to the Black Sea via the Caspian Pipeline Consortium system. S&P Global reported that Kazakhstan sees no “major problems” with the CPC crude route even as regional tensions rose, underlining that this lifeline to European refiners remained open.

Put simply, Europe’s main suppliers either do not depend on Hormuz at all or have alternate routes that were in active use while the public was told the global oil artery had been cut. The picture on the ground was messy and dangerous. It was not the neat all‑or‑nothing blockade invoked in politics and television talk shows.

How benchmarks turned fear into instant price hikes

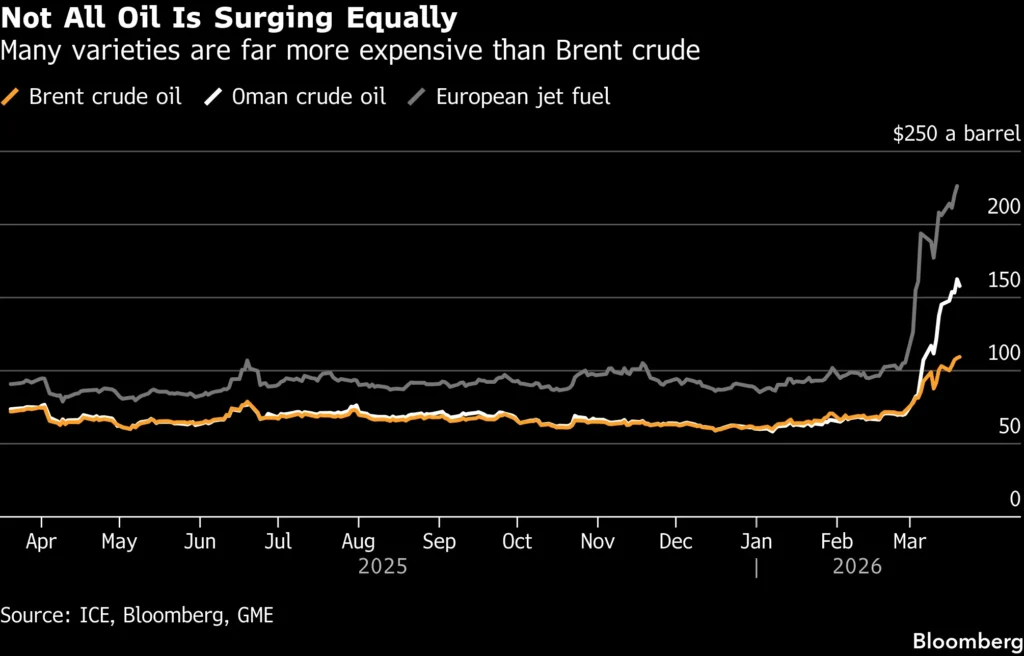

If the physical story was more nuanced, the price story was brutal. Brent, the benchmark that anchors much of the world’s crude trade, became a lightning rod for every rumour and headline.

On 1 March, Reuters reported that oil jumped as conflict grips the Middle East, with Brent up more than six per cent in a single day as US and Israeli strikes on Iran intensified and markets began to price a wider regional war. By the end of the first week, CNBC noted that oil surges 35% this week for the biggest gain in futures trading history, putting the weekly move in historic territory.

IMAGE: Latest Oil Market News and Analysis for March 2 – Look at European jet fuel! (Source: Bloomberg)

The Federal Reserve Bank of St Louis publishes daily Crude Oil Prices Brent – Europe, which shows Brent jumping from the high seventies at the end of February to above 120 dollars by 27 March. Another Reuters story on 3 March, Global oil and gas prices soar as Iran crisis disrupts shipping, linked that move to tanker delays and shut‑in capacity, but also warned that markets were pricing in worst‑case scenarios.

By late March, options traders were betting openly on extreme outcomes. Reuters reported that with Hormuz still shut, options market signals rising risk of 150 dollar oil, as investors paid up for contracts that would profit if Brent spiked to that level.

The European Central Bank has examined this dynamic in its own box on speculation in oil and gas prices in times of geopolitical risks, noting that non‑commercial positioning and derivatives trading can amplify price swings around geopolitical shocks even when underlying supply and demand change more slowly. On the US side, the CFTC’s Commitments of Traders Long Report – Petroleum shows that a small number of large traders control a majority share of gross positions in key crude futures, underlining how concentrated these markets are.

Then came a telling reversal. On 31 March, Reuters wrote that WTI and June Brent crude futures settled down on reports that Iran may move toward ending the war, noting that the May Brent contract was still up roughly 64% for the month but fell on hints of diplomatic movement. The next day, Reuters reported that oil slides after Trump says the US will end its war on Iran soon.

Pipelines do not restart in hours. Tankers do not jump from one sea to another overnight. Yet benchmark prices snapped lower within a day when the narrative shifted from escalation to potential ceasefire. That pattern looks less like slow physical adjustment and more like a paper market that had overshot on fear and then repriced violently when the political script changed.

Whales and the casino behind the crisis

France Soir’s investigation gestured toward speculation but stopped short of naming concrete players. On‑chain data allows us to go further. While European households were told to accept higher prices as wartime duty, a cluster of whales was treating the oil spike as a high‑stakes trade.

On 9 March, on‑chain analysts at Lookonchain spotted a Hyperliquid wallet with the address 0x985f02b19dbc062e565c981aac5614baf2cf501f. Binance Square carried the story under the title Whale deposits 9.5 million USDC into HyperLiquid to short oil 20x, describing how the wallet had sent 9.5 million USDC to Hyperliquid and opened short positions worth about 8.17 million dollars in a tokenised crude contract labelled xyz CL and 6.15 million in a Brent contract labelled xyz BRENTOIL using roughly twenty times leverage.

The following days brought more. TechFlow summarised Lookonchain’s monitoring in a piece titled An address deposited 4 million USDC into Hyperliquid to keep shorting oil, explaining that the same wallet had added another four million USDC and now held about 35 million dollars in combined crude and Brent shorts with unrealised losses already near 1.87 million dollars as prices moved against it. PANews carried a similar account under Crude oil surges 25%, Hyperliquid faces a critical on‑chain situation, noting that tokenised oil volume on Hyperliquid had briefly surpassed Ethereum.

The story reached the English‑language crypto mainstream in reports such as ForkLog’s Tokenized oil surpasses Ethereum on Hyperliquid exchange and CoinDesk’s article A single crypto trader is sitting on a 194 million dollar bet, which mentioned the same oil shorts as part of a wider macro gamble.

As the crisis deepened, Hyperdash‑based accounts that track Hyperliquid traders started publishing regular updates. The profile @hyperdashtrades highlighted rising exposure and losses in posts such as this 17 March update, which put the crude short alone near 23.6 million dollars, and a 23 March update that estimated total oil shorts around 47.7 million dollars across crude and Brent with combined floating losses around three million.

Our own capture of the wallet’s Hypurrscan perps page confirms the scale in one snapshot. It shows a short of roughly 200,000 BRENTOIL contracts valued above 21.6 million dollars and a crude short of about 91,900 CL contracts worth almost 9.9 million dollars, alongside large shorts in HYPE, PUMP, APT, ASTER and other tokens. This is not a small retail trader misclicking on a phone. It is a concentrated macro bet that oil will crash once the panic burns out.

Figure 1. Hyperdash crude‑oil short

Hyperdash portfolio view showing a large crude‑oil short position of approximately 17.18 million dollars in xyz:CL, with size around 169,790 contracts, entry price near 94.43 dollars, mark price just above 101 dollars and liquidation price around 139.17 dollars, backed by roughly 7.04 million dollars in margin. The position is displayed on a Hyperdash performance chart for March 2026, illustrating the scale and volatility of leveraged oil bets during the Iran–Hormuz crisis. Source: internal screenshot consistent with exchange reporting on a 17 million dollar oil short with liquidation price 139 and related coverage on oil shorts on Hyperliquid)

Figure 2. Hypurrscan perps page for 0x985f

Hypurrscan perpetuals page for wallet 0x985f02b19dbc062e565c981aac5614baf2cf501f, showing simultaneous short positions in xyz:BRENTOIL and xyz:CL along with a broader macro short book across multiple tokens. In the captured state, the wallet holds approximately 200,000 BRENTOIL contracts worth about 21.6 million dollars and around 91,900 CL contracts worth about 9.9 million dollars, with significant unrealised losses on both as prices move higher. This visual confirms that the address identified by on‑chain monitors as “oil bear 0x985f” is running a very large leveraged oil‑short strategy on Hyperliquid. (Source: Hypurrscan address view for 0x985f02b19dbc062e565c981aac5614baf2cf501f, consistent with on‑chain monitoring from Lookonchain and PANews)

Together, Figure 1 and Figure 2 show that we are not dealing with abstract “speculators” but with identifiable wallets running system‑sized, high‑leverage oil shorts whose fate could turn on a single war headline. As mainstream finance largely slept through weekends, the panic migrated into tokenised markets. A Hyperliquid co‑founder told Yahoo Finance that the exchange “stands out due to its liquidity, cost‑effectiveness, and rapid innovation” as it cleared more than 500 million dollars of oil trades in a single day, while Fortune noted that one tokenised crude contract reached “nearly 1.7 billion dollars” in 24‑hour volume, about 250 times pre‑war levels. You can find those remarks in How Hyperliquid became an Iran war winner and in Fortune’s piece on why oil traders are rushing to trade on Hyperliquid.

At the same time, exchange news outlets were reporting even more extreme single‑position bets. Gate described how a whale establishes a 17 million dollar oil short position, with a liquidation price of 139, sharing a Hyperdash screenshot of a CL short whose size and liquidation level closely resemble the one we have examined. We cannot yet prove that this specific 17‑million position belonged to 0x985f rather than another whale in the same cluster. What matters is that such bets existed at the core of the crisis.

In plain language, a whale here is simply a trader with huge capital. A short is a bet that prices will fall. A liquidation price is the line where, if the market moves the wrong way, the platform forcibly closes the position, and the trader loses their margin. When oil moves twenty or thirty per cent in a week, a single headline can make or erase millions for these players. For a nurse in Marseille or a truck driver in Bratislava, the only visible effect is the new number on the pump.

Who quietly won while households paid

In a financialised oil system, the pain and the gain rarely sit in the same place. On one side of the ledger are households and small businesses. A typical family driving fifteen thousand kilometres a year in a petrol car can easily face an extra 1,200 to 1,800 euros in annual fuel costs when prices jump by sixty to eighty cents per litre, a scale of hit reflected in EU statistics on energy‑driven inflation in 2026. The Parliament’s own plenary round‑up for March 2026 lists tackling energy price spikes as one of the main concerns.

IMAGE: In Germany, new fuel price law prompts huge midday spike (Source: DW)

On the other side of the ledger are producers, refiners and traders whose profit and loss statements move in the opposite direction. Reuters reported in April 2025 that Exxon signals higher oil, gas prices will help boost Q1 profit, estimating that stronger prices would increase upstream earnings by about 900 million dollars relative to the prior quarter, and improved refining margins would add another 300 to 700 million. A later Reuters story from January 2026, Exxon beats Wall Street targets for Q4 profit with help from lower‑cost oil production, noted that downstream profit had climbed to 2.9 billion dollars thanks in part to better refining economics.

European firms were not bystanders. In late March, TotalEnergies announced that it would extend its price caps at its service stations in France until April 7. The company capped pump prices at 1.99 euros per litre and extended preferential deals for certain electricity and gas customers. That press release is clear proof that prices at the pump are not carved in stone by international markets. When a major energy company chooses to absorb or redistribute part of the shock, it can, at least for some customers.

Compare that to the political reaction. In Australia, Prime Minister Anthony Albanese used his office to announce a temporary halving of the fuel excise and removal of road charges for heavy vehicles, a move documented in his Address to the Nation. Local coverage explained that this meant an immediate reduction of 26.3 Australian cents per litre for three months. In Europe, the Commission’s response centred on urging citizens to work from home, drive less and accelerate the green transition. It did not impose crisis‑time windfall levies specifically aimed at the spike. It did not legislate retail fuel price caps based on pre‑war benchmarks for a defined emergency period. It did not even launch a visible inquiry into whether wholesale price formation had been artificially amplified.

Outside the European bubble, some large buyers were less exposed to this financialised cage. Reuters reported as early as 2012 that Iran accepts Chinese yuan in exchange for oil, and later in 2022 that China buys more Iranian oil now than it did before sanctions. Those arrangements sit outside the dollar‑Brent nexus that Europe chose to remain locked into.

The result was a one‑way transfer. Financial markets turned war panic into higher benchmarks. Benchmarks turned into higher pump prices. Households paid. Oil majors, refiners and well‑positioned traders booked the upside.

Europe had tools and chose not to use them

It is not true that Europe lacks legal weapons against financial abuse in energy markets. The EU’s regulation on Wholesale Energy Market Integrity and Transparency, usually known as REMIT, prohibits insider trading and market manipulation in wholesale electricity and gas. The Agency for the Cooperation of Energy Regulators sets out how these rules apply in its ACER Guidance on REMIT application. That document explains that manipulation includes giving false or misleading signals about supply, demand or prices and securing prices at artificial levels, including through collusive behaviour or abusive use of benchmarks.

IMAGE: European Union flags in front of the European Parliament building in Brussels (Source: AI-generated)

ACER’s page on REMIT investigations and enforcement decisions shows that such breaches can lead to sanctions at the national level. A separate Energy Community note on market manipulation under REMIT stresses that abusive strategies designed to move prices away from fundamentals can fall under the regulation. In 2025, the Commission also updated the fee framework for ACER’s supervision under a decision summarised in its press item on new EU rules on REMIT fees, underlining that the watchdog is expected to play an active role.

The March summit itself underlined the political priorities. In its Brussels plenary newsletter, the Parliament stressed plans to use Emissions Trading System revenues and long‑term climate tools to ease the burden, rather than direct regulation of fuel prices or aggressive enforcement against speculative excess. At the same time, ECB officials told Reuters that a temporary oil spike from the Iran conflict “should not significantly alter the medium‑term inflation forecast or necessitate a policy response,” and Christine Lagarde said the situation was “not comparable to the 2022 crisis,” as summarised in Iran war fuels central bank rate hike bets and in ECB on Alert as Iran War Drives Energy Prices. The message from Frankfurt was that the shock was serious but manageable.

Across the Atlantic, American officials were at least willing to say out loud that future behaviour mattered. Reuters reported that the White House was weighing oil futures market action to combat price spikes, and another Reuters piece quoted the CFTC’s enforcement chief naming insider trading in prediction markets as a supervisory priority in a discussion that also touched on energy markets.

Meanwhile, the global monetary architecture magnified Europe’s vulnerability. A 2018 Reuters analysis on Iran oil sanctions and China’s “petro‑yuan” noted that forcing sanctioned producers out of the dollar system pushes them toward alternative currency arrangements. Europe, by contrast, chose to remain tied to dollar‑denominated Brent benchmarks and the petrodollar system even as this made its economies more exposed to US‑centric financial shocks.

In Europe, there has so far been no public announcement of a major REMIT case or EU enforcement action targeting oil‑linked market abuse during the Iran war spike. The agency with a mandate to police artificial pricing in wholesale energy markets (ACER) remained invisible while Brent swung by double digits on war headlines, and whales on Hyperliquid built tens of millions of dollars in leveraged bets on the outcome.

No one seriously claims that every price move in March 2026 was fraudulent. Physical risks were real, tankers were delayed, producers diverted flows to new routes, and the war brought genuine supply uncertainty. However, the indictment lies elsewhere. European leaders chose to present the shock as a simple act of nature, a punishment delivered by Iran and geology, when their own documents admit that Europe’s direct dependence on Hormuz is limited and that the main channel of impact was the financial system and its benchmarks. They allowed a market architecture that rewards volatility and high leverage to set the prices paid by hundreds of millions of citizens without deploying the investigative and regulatory tools that exist on paper.

What Europe experienced was not an unavoidable crisis of black gold. It was a political choice to let a financialised oil system weaponise a distant war against European living standards. The whales, the benchmarks and the companies knew how to navigate that system. Ordinary people were told to take shorter showers and drive less.

READ MORE IRAN NEWS AT: 21st Century Wire IRAN Files

SUPPORT OUR INDEPENDENT MEDIA PLATFORM – BECOME A MEMBER @21WIRE.TV

VISIT OUR TELEGRAM CHANNEL

21st Century Wire is an alternative news agency designed to enlighten, inform and educate readers about world events which are not always covered in the mainstream media.

Source: https://21stcenturywire.com/2026/04/02/the-hormuz-hype-how-europe-got-played-at-the-oil-casin/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,800,148,822 |

| Stories: | 8,628,655 |

Whistler Blowers, Insiders